GST In Singapore

GST In Singapore

ACHI BIZ is your personalized premium service provider when it comes to seeking business management assistance in Singapore.

ACHI BIZ provides with our experts for the taxation services such as for GST, individual Income Tax and Corporate Income Tax for all types of Firms and Entities in Singapore.

Goods and Services Tax (GST): What It Is and How It Works

Businesses Required to Register for GST

If your business does not exceed $1 million in taxable turnover, you may still choose to voluntarily register for GST after careful consideration.

Please refer to IRAS webpage at www.iras.gov.sg for more information on whether you need to register for GST.

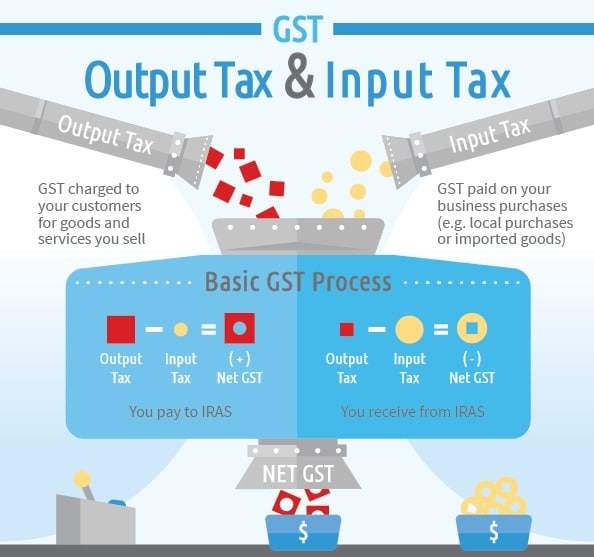

Charging and Collecting GST

The GST that you incur on business purchases and expenses (including import of goods) is known as input tax. If your business satisfies the conditions for claiming input tax, you can claim the input tax on your business purchases and expenses.

This input tax credit mechanism ensures that only the value added is taxed at each stage of a supply chain.

Paying Output Tax and Claiming Input Tax Credits

As a GST-registered business:

- You must submit your GST return to IRAS one month after the end of each prescribed accounting period. This is usually done on a quarterly basis.

- You should report both your output tax and input tax in your GST return.

- The difference between output tax and input tax is the net GST payable to IRAS or refunded by IRAS.

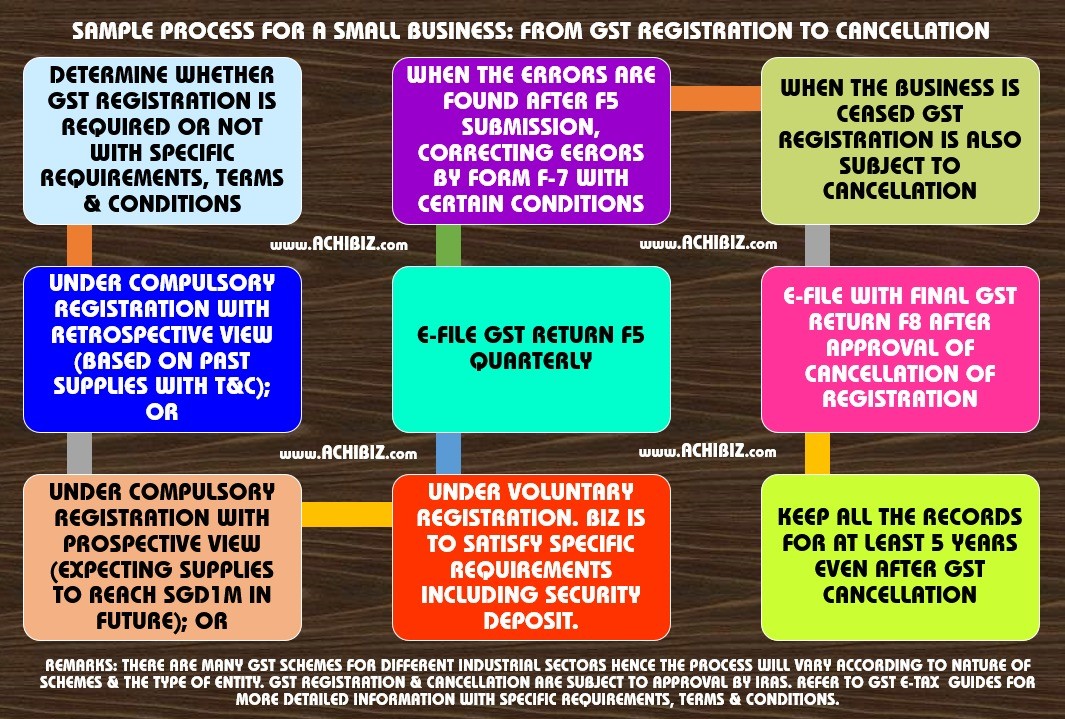

Refer to the below links for GST e-Tax Guides from registration till cancellation with Sample Illustration Guide for more information (source from IRAS):

|

GST Schemes

There are two types of GST Schemes viz. General Scheme & Industry-Specific Scheme available in Singapore with their own features, requirements, Terms & Conditions.

General Scheme |

Cash Accounting Scheme

|

Discounted Sale Price Scheme

|

Gross Margin Scheme

|

Hand-Carried Exports Scheme (HCES)

|

Import GST Deferment Scheme (IGDS)

|

Major Exporter Scheme (MES)

|

Tourist Refund Scheme (TRS) for Businesses

|

Zero GST (ZG) Warehouse Scheme

|

Industry-Specific Scheme |

Approved Contract Manufacturer and Trader (ACMT) Scheme

|

Approved Import GST Suspension Scheme (AISS) (For Aerospace Players)

|

Approved Marine Customer Scheme (AMCS)

|

Approved Marine Fuel Trader (MFT) Scheme

|

Approved Refiner and Consolidator Scheme (ARCS)

|

Approved Third Party Logistics (3PL) Company Scheme

|

Specialised Warehouse Scheme (SWS)

|

Rectification / Amendment of errors in GST Return in Singapore:

You may request for a GST F7 for the affected prescribed accounting period at myTax Portal to disclose the errors made. Please complete the GST F7 with the revised figures (including all adjustments) for all boxes as it will supercede the previous GST return (GST F5 or a previous GST F7) submitted for the accounting period.

However, depending on the nature and amount of the error made, you may be allowed to adjust for the error in your GST F5 for the next accounting period.

Correcting Errors in Your GST Return:

If you have made errors in your submitted GST F5/ F7/ F8 forms, you should file GST F7 to correct the errors.

Administrative Concession by IRAS for Correcting Errors:

As an administrative concession, you may choose to adjust for the errors made in your next GST F5 if you meet both of these criteria:

- The Net GST amount in error (i.e. output tax error – input tax error) for all the affected prescribed accounting periods is not more than $1,500; and

- The total non-GST amounts in error for (each of) the affected accounting period(s) is not more than 5% of the total value of supplies declared in the submitted GST return (i.e. Box 4). In the case where there was no supply made in the affected accounting period, the 5% rule applies to the total value of the taxable purchases (i.e. Box 5).

However, the administrative concession does not apply to:

- Errors that affect Boxes 9 to 12 of your past GST F5.

- Errors made in your last return, GST F8.

GST payable on overseas digital services from 1 Jan 2020

From 1 Jan 2020, GST is chargeable on digital services bought from GST-registered overseas service providers.

Here’s what you need to know as a digital consumer:

- From 1 Jan 2020, GST is chargeable on movie and music streaming services, as well as other digital services bought from GST-registered overseas providers.

- Digital services provided by overseas providers include downloadable digital content, subscription-based media, software programmes, web hosting services, etc.

- Note: Not all overseas service providers can charge GST. Be vigilant!

- Check whether an overseas provider is registered at https://go.gov.sg/gstlistingsearch

Under the OVR regime, overseas digital service providers with a yearly global turnover of more than S$1 million that sell more than S$100,000 worth of digital services to customers in Singapore in a 12-month period are required to register for GST and charge GST.

Examples of digital services purchased from overseas service providers include:

Meanwhile, there will be no changes in the GST treatment for online purchases of goods: GST remains payable on all goods imported into Singapore, with the exception of goods valued S$400 and below imported via air or post.

What consumers need to do

As overseas digital service providers use information such as payment and billing information to determine if customers reside in Singapore, businesses and consumers are responsible for providing complete and accurate information to registered overseas digital service providers. It is a serious offence to provide incorrect or false information to overseas digital service providers to avoid paying GST on digital services.

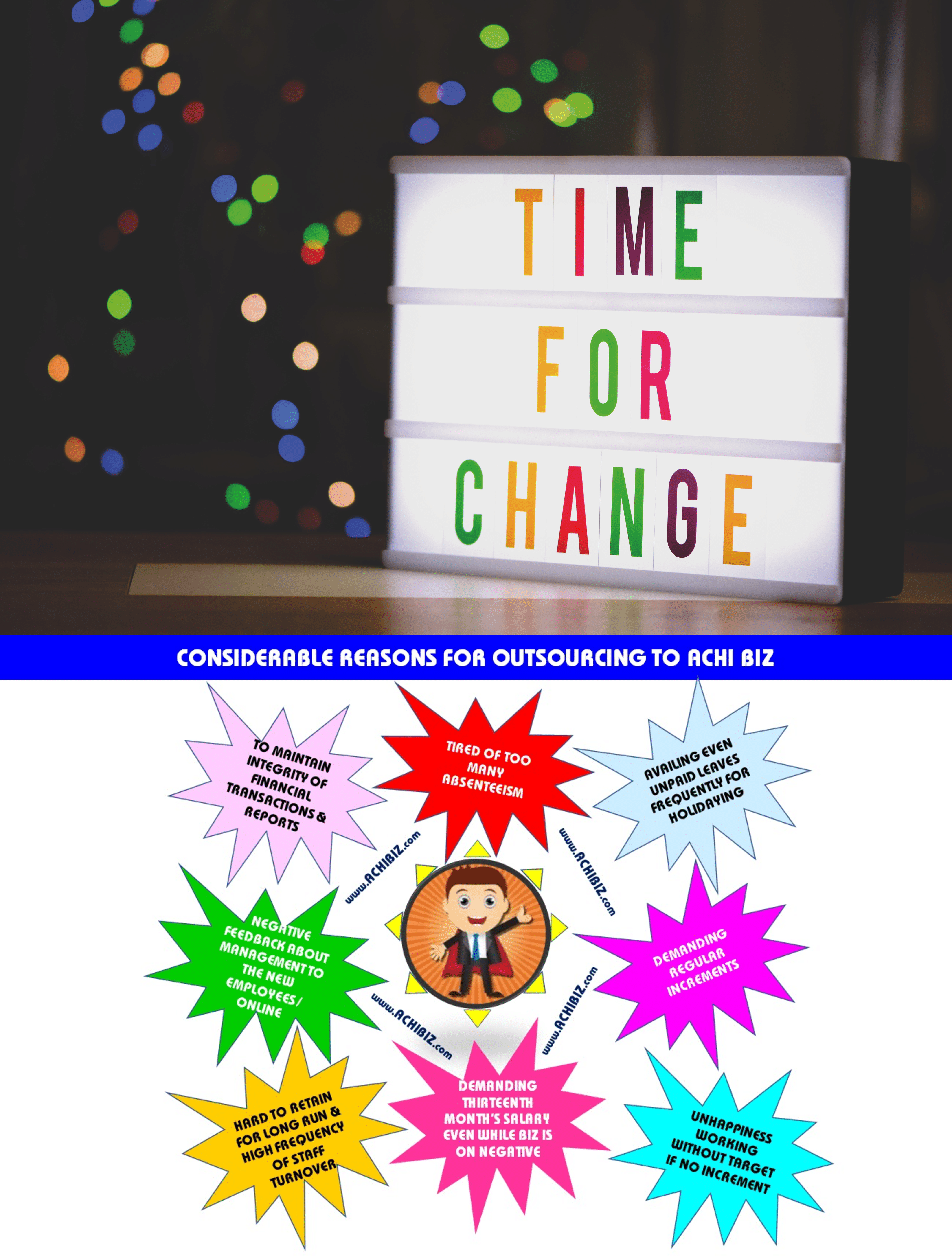

When you encounter with any of the following issues with your Book-Keeping &/or Accounting staff then we strongly suggest you to consider for outsourcing to ACHI as our costs are fixed basis per annum:

When you encounter with any of the following issues with your Book-Keeping &/or Accounting staff then we strongly suggest you to consider for outsourcing to ACHI as our costs are fixed basis per annum:

- To maintain the integrity of your financial positions & reports

- Tired of too many absenteeism

- Availing even unpaid leave for frequently for holidaying

- Demanding regular increment

- If there is no increment then working with unhappiness & with no target

- Demanding Thirteenth month salary & bonus even while your business is on negative

- Hard to retain for long run

- Negative feedback about your management to the new employees or online