24/7/365

24/7/365

Differences between a solvent and insolvent EPC

A private company can have not more than 50 members. An exempt private company (EPC) can be a private company with less than 20 members, and does not have any corporations holding beneficial interest in its shares (whether directly or indirectly). An EPC can also be a private company owned by the Government that is declared in the Gazette to be an EPC.

- An EPC is insolvent if it is unable to meet its debts when they are due. Insolvent EPCs are required to file financial statements as mentioned above.

- Solvent EPCs only need to make an online declaration of their solvency, and filing financial statements are voluntary.

Prepare Financial Statements Highlights

Not all companies are required to file a full set of financial statements in XBRL format. Some companies are only required to file financial statements highlights in XBRL format, with a PDF of the financial statements tabled at the AGM. Refer to the above Table whether your company is eligible only to file financial statements highlights in XBRL format.

Applying for Exemptions from XBRL Filing Requirements

Companies may apply for exemption from XBRL filing requirements from ACRA, for the following:

- Exemptions from specific business rules in filing your financial statements in XBRL format (e.g. removing the requirement for comparative periods in your financial statement, given valid reasons).

- Exemption from filing full set of XBRL financial statements, and instead filing Financial Statement Highlights (FSH) in XBRL format only, if you have valid proof that the full set of XBRL financial statements cannot be prepared.

- Allowing you to file PDF copy of financial statements, with valid proof that you cannot file the full set of XBRL financial statements, or FSH.

Exemptions are evaluated on a case-by-case basis by ACRA.

Some Important Frequently Asked Questions on filing of ARs:

Some Important Frequently Asked Questions on filing of ARs:

Q: What if a company fails to file its Annual Returns?

A: Enforcement actions will be taken against directors and companies for annual returns filing breaches.

Q: What are some of the transactions that would be disregarded in determining whether a company is dormant?

A:

- The appointment of a secretary of the company;

- The appointment of an auditor;

- The maintenance of a registered office;

- The keeping of registers and books under certain sections of the Companies Act;

- The payment of fees or charges payable under any written law;

- The taking of shares in the company by a subscriber to the Constitution in pursuance of an undertaking of his in the Constitution.

For more details, please refer to s205B of the Companies Act.

Q: My company’s financial statements are exempted from audit, but we have chosen to get our financial statements audited. Should we be filing the unaudited or audited financial statements?

A: Companies that are exempted from audit requirements are not required to have their financial statements audited. Instead, they will prepare unaudited financial statements for purposes of AGMs and filing with ACRA. If the company chooses to have the financial statements audited, it will submit the audited financial statements together with the auditor’s report.

Q: If the company has already filed an Annual Return with ACRA, does it still need to file any documents with IRAS?

A: For a dormant company:

- The company must submit its Income Tax Return (Form C) unless it has been granted a waiver from IRAS. The company may apply for a waiver from IRAS by submitting the form ‘Application for a Waiver to Submit Income Tax Return (Form C) by a Dormant Company.

For all other companies:

- The company which has filed Annual Return with ACRA must also file its Income Tax Return (Form C-S / Form C) and the necessary supporting documents (such as financial statements and tax computation) with IRAS annually.

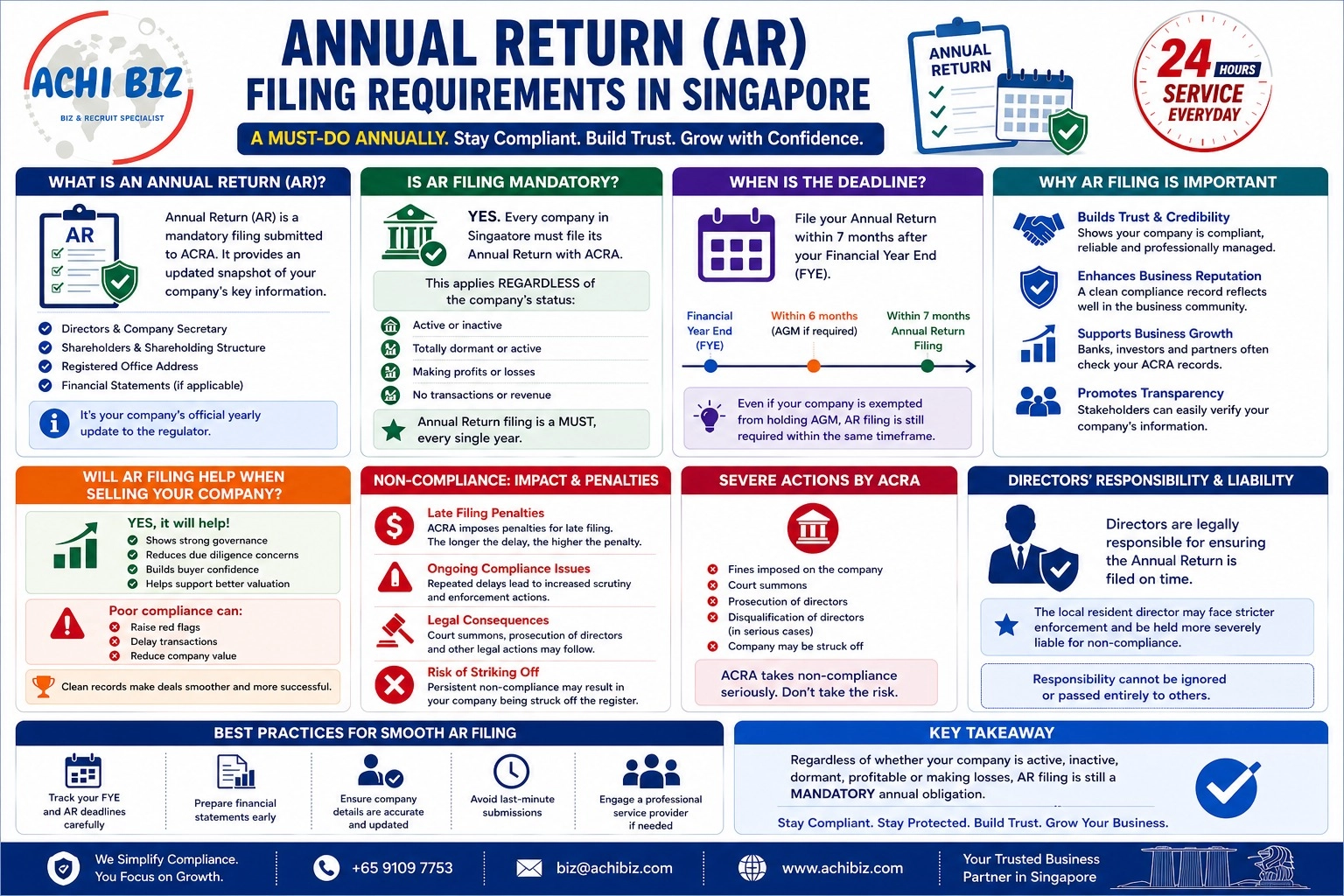

❓ What is an Annual Return (AR) in Singapore?

👉 An Annual Return is a mandatory filing submitted to ACRA that provides updated information about a company, including directors, shareholders, registered address, and financial statements (if applicable).

❓ Is Annual Return filing mandatory for all companies in Singapore?

👉 Yes, all companies must file their Annual Return with ACRA every year, regardless of their business activity or financial performance.

❓ Do dormant companies need to file Annual Return in Singapore?

👉 Yes, even if a company is dormant with no transactions or income, it is still required to file its Annual Return annually.

❓ Do companies with no profit need to file Annual Return?

👉 Yes, companies must file AR even if they are making losses or have no revenue. Filing is based on company registration, not profitability.

❓ When is the deadline for filing Annual Return in Singapore?

👉 A Pte Ltd company must file its Annual Return within 7 months after its financial year end (FYE).

❓ What happens if a company files Annual Return late?

👉 Late filing will result in penalties imposed by ACRA, and repeated delays may lead to further enforcement actions.

❓ What are the penalties for not filing Annual Return?

👉 Non-compliance may lead to fines, court summons, prosecution of directors, and possible striking off of the company.

❓ Who is responsible for filing the Annual Return?

👉 The directors are legally responsible for ensuring that the Annual Return is filed on time. The local resident director may face stricter enforcement.

❓ Why is Annual Return filing important?

👉 It ensures compliance, keeps company records updated, builds trust with stakeholders, and supports transparency in the business environment.

❓ Does Annual Return filing help when selling a company?

👉 Yes, proper and consistent AR filing improves credibility, reduces due diligence concerns, and increases buyer confidence during a sale.

❓ Can a company be struck off for not filing Annual Return?

👉 Yes, persistent failure to file AR may result in the company being struck off by ACRA.

❓ What information is included in an Annual Return?

👉 It includes details such as company officers, shareholders, registered address, and financial statements where required.