Tax Clearance (IR21)

Tax Clearance for Foreign & SPR Employees (IR21) In Singapore

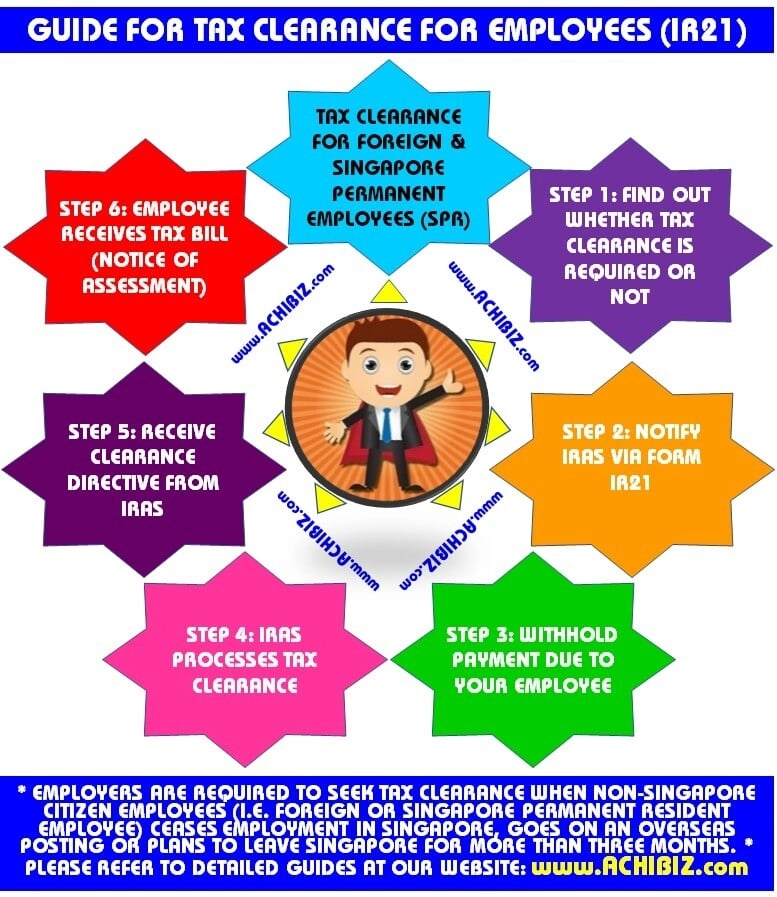

Generally, when your non-Singapore Citizen employee (i.e. foreign or Singapore Permanent Resident employee) ceases employment with you in Singapore, goes on an overseas posting or plans to leave Singapore for more than three months, you are required to seek tax clearance for him. As an employer, you have the responsibility to file the Form IR21 and withhold all monies due to the employee for tax clearance purpose.

This applies to all work pass holders including Personalised Employment Pass (PEP) holders.

You may wish to visit IRAS online for detailed information and current updates.

Step 1: Find Out Whether Tax Clearance is Required

Use the Tax Clearance Calculator (68KB) to find out whether you are required to seek tax clearance for your non-Singapore Citizen employee. Proceed to the next step only if tax clearance is required.

Step 2: Notify IRAS via Form IR21

File the Form IR21 at least one month before your non-Singapore Citizen employee ceases employment with you in Singapore, goes on an overseas posting or leaves Singapore for more than three months.

If you are not able to give one month’s notice, please provide IRAS with the reason in the Form IR21. Unless there are valid reasons (e.g. an employee’s immediate resignation), employers who do not file or are late in filing the Form IR21 may be liable to a fine of up to $1,000.

Tips/Pointers

- File the Form IR21 electronically at myTaxPortal for faster tax clearance. To use this e-Service, you need to be authorised by your organisation via the Singapore Corporate Access (CorpPass). If you are new to e-Filing, you can view our e-Learning video or refer to the following user guides on our e-Services:

- View tax clearance notices/letters.

- View sample Letter Of Undertaking (LOU) to be obtained from PR Employees.

- When completing the Form IR21, you should include the income your employee earned in the year of cessation or departure, as well as that earned in the preceding year if that has not been transmitted electronically to IRAS via the Auto-Inclusion Scheme (AIS) at the point of tax clearance.

- Severance payments that constitute compensation for loss of office may not be taxable. You should provide IRAS with the necessary information for evaluation.

- Gratuity for past services payable at the end of contract is taxable.

- Payments to employees for salary in lieu of notice is taxable.

- If the employee has unexercised share options or unvested share awards, he will be deemed to have derived gains from these share options or share awards at the point of tax clearance under the “deemed exercise” rule. This also applies to those with selling restrictions. For details on how to report share option/share award gains in the Form IR21, please refer to “What to do if there are unexercised stocks options?”.

Step 3: Withhold Payment Due to Your Employee

You are also required to withhold all monies (overtime pay, leave pay, allowances, reimbursements, gratuities, lump sum payments, etc.) due to your employee from the date you are aware of the employee’s impending cessation of employment or departure from Singapore.

If you are unable to withhold all monies from your employee, please provide IRAS with the reason in the Form IR21. Otherwise, you may be liable for the tax that is owed by the employee.

Step 4: IRAS Processes Tax Clearance

Generally, 80% of e-Filed Form IR21 will be processed within 7 working days. For paper-filed forms, 80% are processed within 21 days.

Processing time may take longer if the information given in the Form IR21 is incomplete or when IRAS needs to seek clarification on the submitted information.

You can check the status of tax clearance at myTax Portal .

If you need to make changes to the income details provided in your earlier Form IR21 submission, please file another Form IR21 and indicate an appropriate Form IR21 type (i.e. “Amended” or “Additional”).

If you are only making changes to the “Amount of Monies Withheld pending Tax Clearance” reported in the Form IR21, please inform IRAS via email or post to Inland Revenue Authority of Singapore, 55 Newton Road, Singapore 307987. You do not need to file an Amended Form IR21.

Step 5: Receive Clearance Directive from IRAS

Upon tax clearance, you will receive either a Directive to Pay Tax or a Notification to Release Monies. The Clearance Directive will be issued to you by post. You will receive it within five to seven working days.

Separately, an electronic copy of the Clearance Directive will be made available at myTax Portal within three working days from the date the Form IR21 is processed.

The Directive to Pay Tax is to inform you of the amount of monies to be remitted to IRAS. The payment needs to be made within 10 days from the date of the Directive to Pay Tax. The Notification to Release Monies is to inform you to release the withheld monies to your employee. However, if you have submitted an Amended/Additional Form IR21, you should not release the withheld monies to the employee until you receive another Clearance Directive in respect of the Amended/Additional Form IR21.

Step 6: Employee Receives Tax Bill (Notice of Assessment)

Your employee will receive a tax bill via post. The employee will be informed to pay the remaining tax if the amount of monies withheld by you is not sufficient to cover his tax. He can also view the electronic copy of his tax bill at myTax Portal which he can access using his SingPass.

Source of Information for Tax Clearance / Declaration & their related matters is from the Inland Revenue Authority of Singapore (IRAS).

Please CONTACT us if you wish to know more about this service or many other services.