Financial Year End (FYE)

Financial Year End (FYE)

Every company in Singapore must always fix the financial activities at the end of the year (FYE). If a company is in form of a subsidiary, its FYE must also coincide with year-end financial statements of its holding company.

When you incorporate a Pte Ltd company in Singapore, one of the first decisions you’ll make is your Financial Year End (FYE). It might seem like a small administrative detail, but it directly affects your bookkeeping, accounting, financial statements, tax filing with IRAS, and compliance with ACRA.

Get it right from the start, and your compliance becomes smoother. Get it wrong, and you’ll spend unnecessary time fixing timelines, chasing deadlines, and dealing with avoidable complications.

What Is Financial Year End (FYE)?

Your Financial Year End in Singapore is the date your company closes its accounts for the year. For example, if your FYE is 31 December, your financial year runs from 1 January to 31 December.

It determines when you prepare:

- Financial statements

- Corporate tax filings

- Annual returns with ACRA

Many businesses simply choose 31 December without much thought. While that works for some, it’s not always the best option.

Choosing the right FYE for your Singapore company helps you:

- Align with your business cycle or industry trends

- Manage cash flow and tax planning better

- Ensure your accounting team has enough time for closing and reporting

- Avoid peak periods when everyone is filing at the same time

For example, if your business is seasonal, setting your FYE after your peak period makes reporting more meaningful and manageable.

Every company in Singapore needs to have an office registered in Singapore that must be open at the same time accessible to the public during the normal office hours.

What Is a Virtual Registered Address in Singapore?

If you’re planning to start a business in Singapore, one thing you’ll definitely need is a registered business address in Singapore. But that doesn’t mean you must rent an office right away. Many businesses today use a virtual registered address in Singapore to stay compliant while keeping costs low.

A virtual registered address Singapore is a legitimate business address you can use for company registration without physically operating there. It’s usually provided by a corporate service provider and used for receiving official correspondence.

Is a Virtual Registered Address Legal in Singapore?

In Singapore, every company must have a registered office address in Singapore where government letters and notices can be delivered. The address must be a real physical location, accessible during normal business hours, and able to receive mail. As long as these conditions are met, using a virtual office address in Singapore is completely legal.

Local Resident Director

Local Resident Director

What Is a “Local Director” in Singapore?

Under Singapore law, every Pte Ltd must appoint at least one director who is ordinarily resident in Singapore, as required by the Accounting and Corporate Regulatory Authority (ACRA).

This local director can be:

- A Singapore Citizen

- A Singapore Permanent Resident (PR)

- An Employment Pass holder (with a valid local residential address)

The key point is simple: your company must have someone locally accountable.

Why This Requirement Exists

This isn’t just red tape. Singapore enforces this rule for practical and legal reasons.

1. Accountability and Responsibility

A local director ensures there is someone within Singapore who can be held accountable for the company’s actions and compliance.

2. Regulatory Communication

Authorities need a reliable point of contact within the country for notices, audits, or enforcement matters.

3.Business Credibility

Having a local director signals legitimacy. It shows that your company has a real presence in Singapore—not just a paper setup.

A director of a company has to comply with a number of statutory obligations under the Companies Act in Singapore.

Some of these key obligations or duties include:

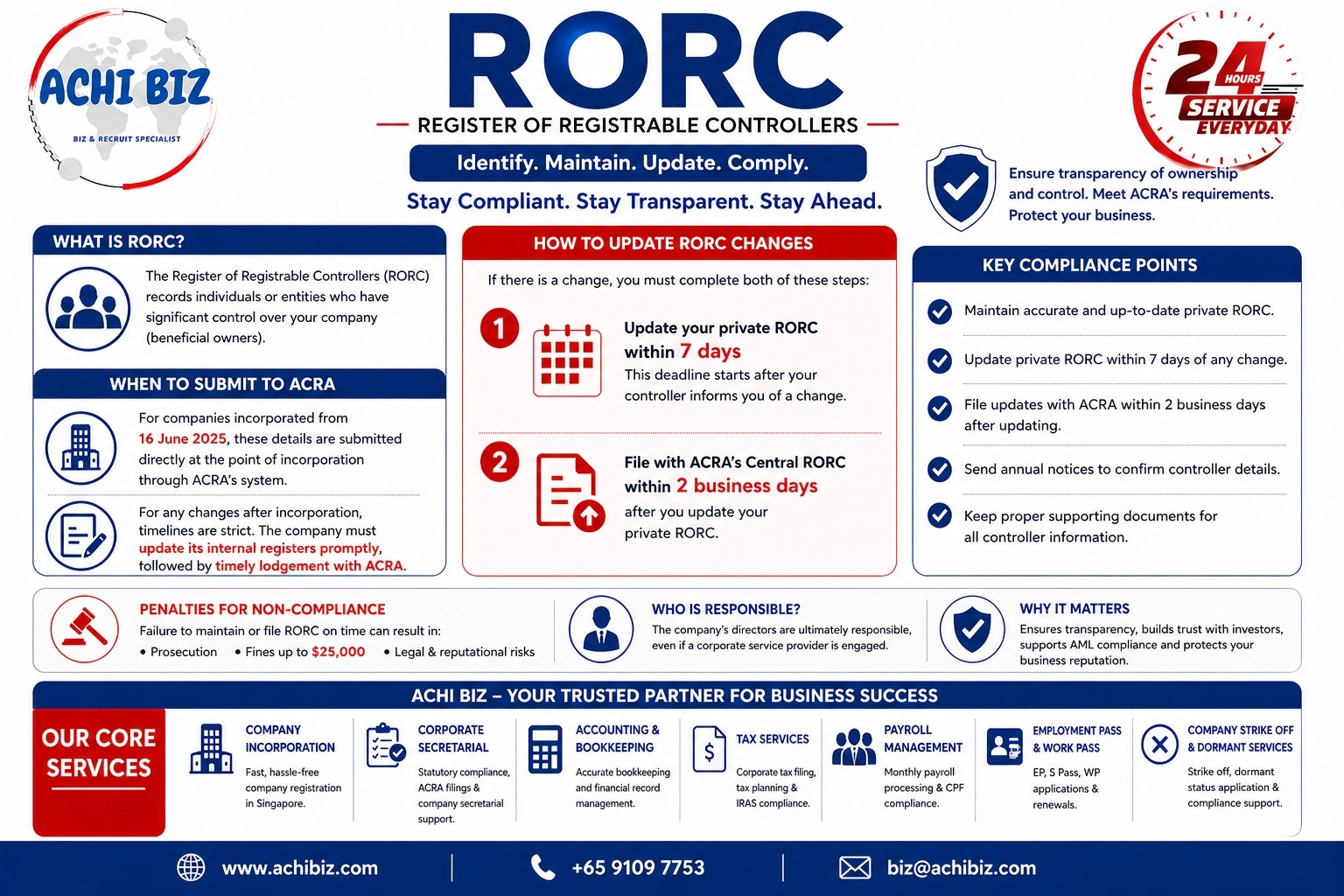

Register of Registrable Controllers

Register of Registrable Controllers

With effect from 31 March 2017, companies, foreign companies and LLPs (unless exempted) are required to maintain beneficial ownership information in the form of a register of registrable controllers, and to make the information available to public agencies upon request.

Filing Requirements of Register of Controllers (RORC) (W.e.f: 30-July-2020)

In line with international practices, ACRA has implemented a new requirement for all companies, foreign companies and Limited Liability Partnerships (LLP), unless exempted, to lodge information on their Registers of Registrable Controllers (RORC) with ACRA via BizFile+ from 30-July 2020 onward.

Companies, foreign companies and LLPs registered on or after 16 June 2025 are to set up their private RORC and file the same information with ACRA on the date of their incorporation or registration.

If there is any update to the controllers’ particulars, companies, foreign companies and LLPs must lodge the change with ACRA within 2 business days after updating the information in their private RORC.

This is in addition to the existing requirements for companies and LLPs to maintain a RORC at the registered office address.

Penalties for not lodging information with ACRA

While there are no late filing fees, failure to lodge RORC information with ACRA may lead to prosecution for the offence and the offender can face a fine of up to $25,000 upon conviction.

Click here for detailed FAQ on RORC.

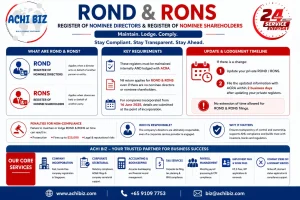

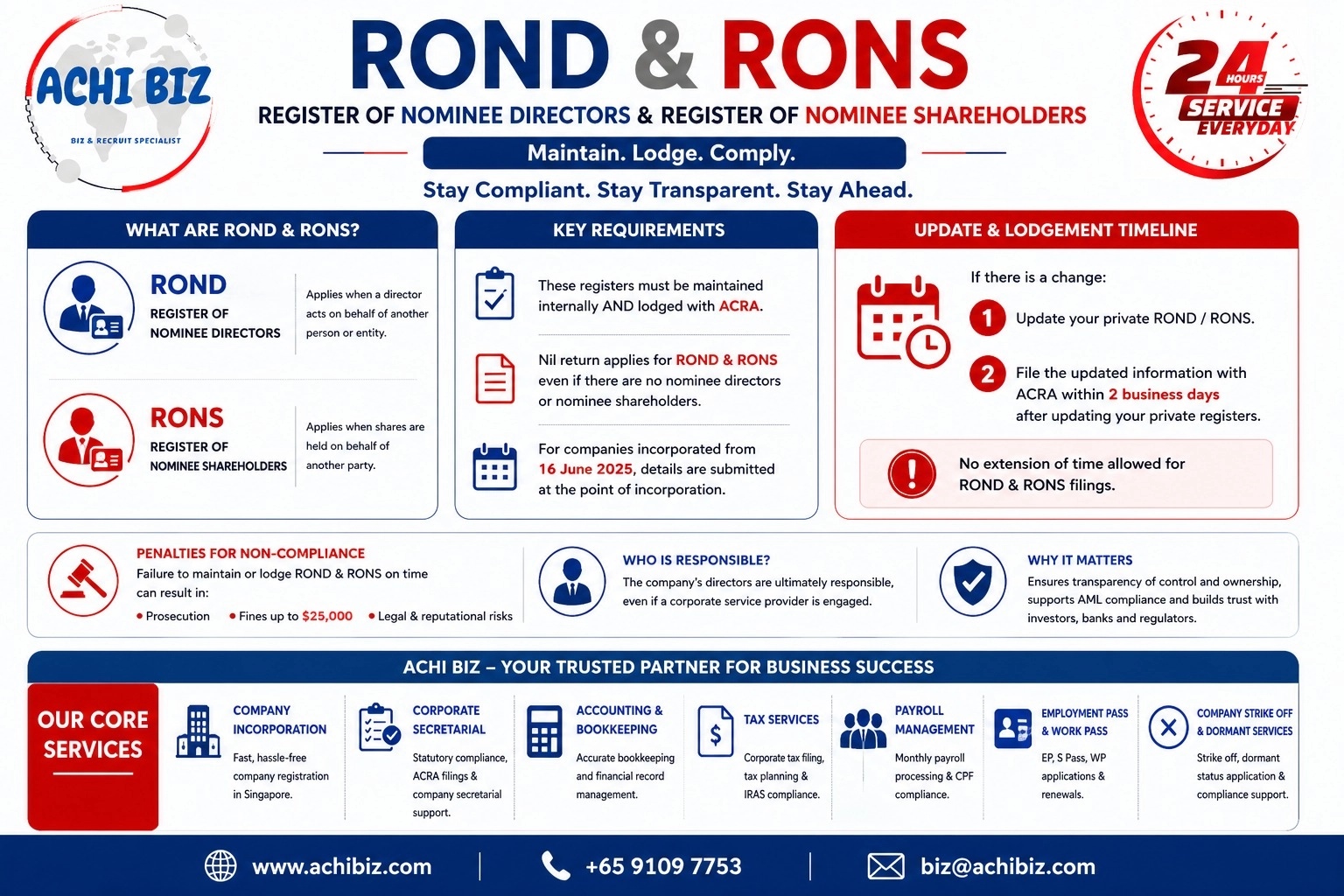

Register of Nominee Directors

With effect from 31 March 2017, Companies are required to keep a register of its nominee directors containing the particulars of the nominators of the company’s nominee directors and produce the register of nominee directors and any related document to the Registrar, an officer of the ACRA or a public agency, upon request.

Register of Nominee Shareholders

Companies in Singapore are required to maintain a Register of Nominee Shareholders (RONS) starting from 05 October 2020. The company must identify nominee shareholders, record both the nominee and nominator (beneficial owner) details, keep the information up to date, and provide it to ACRA upon request.

Filing Requirements of Nominee Directors (ROND) and Nominee Shareholders (RONS) (W.e.f: 16-June-2025)

Filing Requirements of Nominee Directors (ROND) and Nominee Shareholders (RONS) (W.e.f: 16-June-2025)

With effect from 16 June 2025, while companies and foreign companies will continue maintaining their private Registers, they must also submit the information to ACRA’s Central Registers of Nominee Directors and Nominee Shareholders (deadline: 31 December 2025). Following the initial submission, any updates to private Registers held with the companies must be filed with ACRA within 2 business days.

In addition, companies incorporated and foreign companies registered on or after 16 June 2025 with directors and/or shareholders who are nominees on the date of incorporation/registration are required to file information on such nominees and nominators with ACRA at the time of incorporation/registration. To meet this requirement, you will need to lodge the information while applying for incorporation or registration using the “Register new business entity” eService.

Once the information is filed with ACRA’s Central Registers, the nominee status of directors and shareholders will be publicly available and will appear in the business profile of the relevant companies. However, complete information on the particulars of nominators in ACRA’s Central Registers will only be accessible to law enforcement agencies.

Some companies are exempted from maintaining Registers of Nominee Directors (ROND) and Nominee Shareholders (RONS).

Penalties for not lodging information with ACRA

Failure to lodge information with ACRA may lead to prosecution, and the offender can face a fine of up to $25,000 upon conviction.

Register of Members

All companies must maintain with ACRA an electronic Register of Members (EROM), which is a listing of all shareholders. This information is updated whenever a company files a registration of share ownership or changes in share ownership. All companies’ Electronic Registers of Members are available for purchase by members of the public from ACRA.

Electronic Registers of Directors, Secretaries, Auditors and CEOs

Similarly, companies must maintain electronic registers of directors, secretaries, auditors and CEOs with ACRA. Companies are required to update ACRA within 14 days after changes in appointments.

, and core services including company incorporation, employment agency services, immigration services, nominee director & shareholder services, accounting & tax services, and corporate secretarial services.](https://achibiz.com/wp-content/uploads/2026/04/ACHI-SA-Image-0091-Keep-Your-Company-Information-Up-To-Date-200x300.webp) Changes in Company Information / Particulars

Changes in Company Information / Particulars

Companies are required to update ACRA within 14 days of any changes to the company’s name, address and business activity.

Changes in Personal Particulars of Company Officers including Secretaries and Shareholders

Running a Pte Ltd company in Singapore comes with ongoing responsibilities—and one of the most overlooked is keeping your company information and personal particulars of officers up to date.

This includes changes to directors, shareholders, company secretary, registered address, shareholding structure, and personal details such as residential address, passport number, or contact information.

It may sound administrative, but in reality, it’s a core compliance requirement under ACRA. Ignoring it can create serious issues down the line.

What Changes Must Be Updated?

Under Singapore law, companies must update ACRA whenever there are changes to:

- Company information (e.g. business activities, registered address, company name)

- Directors and company secretary details

- Shareholders and shareholding structure

- Personal particulars (e.g. name, address, identification details)

Even small changes—like updating a residential address—must be properly recorded.

worth of paid-up capital (also known as share capital) to register your Singapore Company. This capital amount can be increased at any time after once the company is incorporated.

worth of paid-up capital (also known as share capital) to register your Singapore Company. This capital amount can be increased at any time after once the company is incorporated.

.](https://achibiz.com/wp-content/uploads/2026/04/ACHI-SA-Image-0084-Virtual-Registered-Address-in-Singapore.webp)

, and core services including company incorporation, employment agency services, immigration services, nominee director & shareholder services, accounting & tax services, and corporate secretarial services.](https://achibiz.com/wp-content/uploads/2026/04/ACHI-SA-Image-0091-Keep-Your-Company-Information-Up-To-Date.webp)