General partnership law does not apply to LLPs

A Limited Liability Partnership (LLP) is a business organisation comprising two or more persons associated for carrying on a lawful business with a view to profit that is registered as such under the Limited Liability Partnerships Act (Cap 163A). Despite its name, it is not treated as a partnership and general partnership law does not apply to LLPs.

Legal Identity of LLP is separate legal personality

The LLP is a body corporate that has a separate legal personality. It can sue, be sued and own property in its own name. The LLP is liable for its own debts and the partners and managers of the LLP cannot be made liable for such debts. Each of the partners are assessed and taxed individually on their respective share of the profits in the LLP.

Every partner is agent of LLP but LLP is not bound by unauthorized acts of partners

Every partner of the LLP is regarded as an agent of the LLP. However, the LLP is not bound by the acts of a partner which are not authorised where either this fact is known to the person dealing with the partner or the person does not know or believe the partner to be a partner in the LLP.

Governing relationship by LLP agreement

The relationships amongst partners in an LLP are governed by the limited liability partnership agreement. Matters not covered by the LLP agreement are governed by the provisions of the First Schedule of the Limited Liability Partnership Act.

Methods through which one can cease being member of LLP

A partner in an LLP can cease to be a member of the LLP in accordance with the LLP agreement or, where there is no agreement on the matter, by giving 30 days’ notice to the other members of his intention to leave the LLP.

A partner will also cease to be a partner in an LLP upon death or dissolution. In such an event, the LLP is required to pay to the former partner (or his legal representative or its liquidator) an amount equal to the former partner’s capital contribution to the LLP and the former partner’s share in the accumulated profits of the LLP. The amount is determined as at the date the former partner ceased to be a partner.

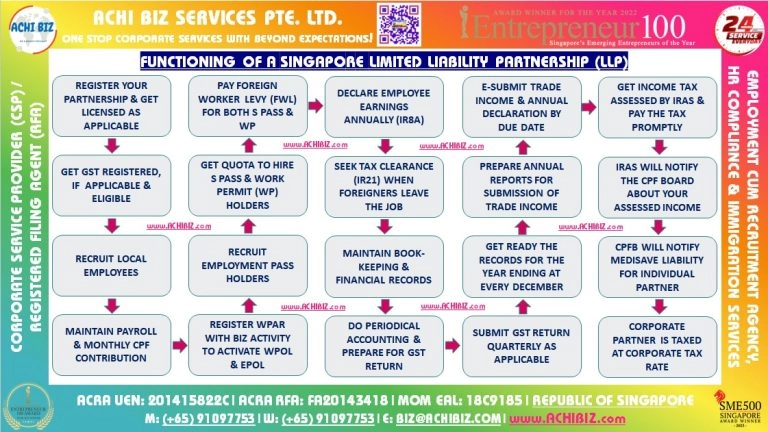

Registration and Compliance

Compliance with the Limited Liability Partnerships Act

Upon registration, LLPs must comply with the provisions of the Limited Liability Partnerships Act and any Rules made under the Act. This includes:

Annual filing of a declaration of solvency or insolvency:

- Under Section 24(1) of the LLP Act, the manager of every LLP is required to lodge a declaration stating whether the LLP is solvent or insolvent (i.e. able to pay off its debts or not).

- Under Section 24(2), the first annual declaration must be lodged within 15 months from the date of the registration of the LLP. Subsequent declarations must be lodged once every calendar year and not more than 15 months after the lodgement of the last declaration.

- If the LLP requires an extension of time to lodge the declaration, it can apply for an extension of time under Section 24(3) of the LLP Act.

Other Compliance:

- Keeping of proper accounts to be made available for inspection by the authorities when required;

- Having a registered office to which all communications and notices may be addressed; and

- Publication of its business name, registration number and limited liability status on it invoices and official correspondences. If the LLP is not carrying on business under its registered name, it must also comply with the provisions of the Business Names Registration Act.

One manager of full age and capacity.

All LLPs must have at least one manager who is a natural person and who is of full age and capacity and need not be a Partner. Such a manager must also be ordinarily resident in Singapore. Managers are persons who are concerned in or who take part in the management of the LLP. They need not be a partner of the LLP.

Manager will be held responsible for non-compliance of the Act

The manager is the person who will be held responsible should the LLP fail to comply with the requirements of the Limited Liability Partnership Act pertaining to:

- The filing of a declaration of solvency under section 24 of the Act;

- The publication of the LLP’s name, registration number and limited liability status on its invoices and correspondence; and

- The registration of any change in particulars of the LLP

Disqualification from acting as Manager of LLP

The following persons are disqualified from acting as a manager of an LLP:

- Undischarged bankrupts (unless they get permission from the High Court or the Official Assignee);

- Persons who are under disqualification from so acting pursuant to an order by the High Court because of their previous role in managing LLPs which have become insolvent or which were wound up on grounds of national security;

- Persons who have been convicted of specified offences; and

- Persons who are disqualified from acting as directors or from being involved in the management of companies under the Companies Act (cap 50).

Winding-Up

Ways of dissolving an LLP

- An LLP will continue to exist until it is dissolved.

- Dissolution often takes place after a process called winding-up has been completed.

- The winding-up may be effected voluntarily upon the resolution of its partners.

- Alternatively, the winding-up may be effected following a Court order being made upon the successful application of the LLP itself, any of its partners (or persons representing their estates), any creditor, the liquidator or the Minister for Finance.

Assets management after dissolution

- During the winding-up, the assets of the LLP will be called in by the liquidator and realised. The money collected will be used to first pay off all the debts of the LLP. Any amounts remaining will be distributed to the partners of the LLP in accordance with the LLP agreement.

- Lower registration cost and easy to set up

- Reduced compliance obligations – general meetings, directors, company secretary, etc., are not required

- Only an annual declaration of solvency or insolvency is required

- LLPs are considered as a separate legal entity from their owners, which means that owners are not responsible for any debts or losses the business incurs

- Easier than Partnerships and Sole Proprietorships to secure funding for the start-up years of the business

- Succession of LLPs are perpetual, until they are struck off or wound up

Here go with categorised advantages of LLP:

🟢 LEGAL PROTECTION & LIABILITY | 🟢 OPERATIONAL FLEXIBILITY- Flexible Internal Structure — Partners

define roles, profit-sharing, and management. - Low Regulatory Burden — Less compliance

compared to companies. - No Board Or Directors Required — No rigid

corporate governance structure. - Easy Entry & Exit Of Partners — Simple

process to add or remove partners. - Minimal Formalities — Reduced

administrative and statutory requirements.

|

🟢 TAX & FINANCIAL ADVANTAGES- No Entity-Level Taxation — LLP itself is

not subject to corporate tax. - Pass-Through Tax Treatment — Partners are

taxed based on their status. - Individual Tax For Natural Persons —

Individual partners taxed at personal income rates. - Corporate Tax For Company Partners —

Corporate partners taxed at prevailing corporate tax rates. - No Double Taxation — Profits taxed once at

partner level only.

| 🟢 BUSINESS & STRATEGIC BENEFITS- Stronger Business Credibility — More

professional image than traditional partnerships. - Ideal For Professional Firms — Suitable

for consultants, accountants, legal firms, etc. - Business Continuity — Operations remain

stable despite partner changes. - Fast & Simple Incorporation — Quick

setup with minimal barriers. - Hybrid Structure Advantage — Combines

flexibility of partnership with liability protection.

|

Click here to learn more about Advantages or Pros of all types of Entities in Singapore.

- Profits are taxed are based on the owner’s income level – this means that as the owner’s income level increases, taxes increase as well due to Singapore’s progressive tax system

- Not eligible for Government funded micro loans.

Here go with categorised disadvantages of LLP:

🔴 LEGAL & LIABILITY LIMITATIONS- No Protection For Personal Negligence — Partners remain liable for their own wrongful acts.

- Liability For Own Actions — Limited liability does not cover personal misconduct.

- Potential Disputes Among Partners — Lack of clear agreements can lead to conflicts.

- 👥Weaker Legal Structure Than Company — Less robust governance compared to companies.

- Difficulty In Enforcing Partner Obligations — Depends heavily on LLP agreement terms.

| 🔴 OPERATIONAL & STRUCTURAL CHALLENGES- No Clear Management Hierarchy — Absence of directors may lead to inefficiencies.

- Dependence On Partner Cooperation — Business success relies on mutual trust and alignment.

- Potential Decision-Making Delays — Consensus-based decisions can slow operations.

- Limited Scalability Structure — Not ideal for large or complex organisations.

- Changes In Partners May Disrupt Operations — Entry/exit of partners can affect stability.

|

🔴 TAX & FINANCIAL DISADVANTAGES- No Corporate Tax Benefits At Entity Level — LLP cannot enjoy corporate tax incentives directly.

- Partners Taxed Individually — Income taxed regardless of profit distribution.

- Corporate Partners Taxed At 17% — Company partners subject to corporate tax rates via Inland Revenue Authority of Singapore.

- Limited Tax Planning Flexibility — Fewer structuring options compared to companies.

- No Retained Earnings Tax Deferral — Profits taxed even if retained within LLP.

| 🔴 BUSINESS & STRATEGIC LIMITATIONS- Lower Perception Compared To Pte. Ltd. — May be seen as less prestigious than a company.

- Difficult To Raise Capital — Cannot issue shares to attract investors.

- Not Suitable For High-Growth Businesses — Limited scalability for expansion-driven ventures.

- Less Attractive To Investors — Investors prefer structured equity ownership.

- Transfer Of Ownership Is Less Straightforward — No share-based transfer mechanism like companies.

|

Click here to learn more about Disadvantages or Cons of all types of Entities in Singapore.