Achi Biz Guides

Company Compliance Guide

Statutory or Mandatory Compliance Requirements for Singapore Companies

Once a Singapore Company is incorporated, it becomes essential to comply with the requirements of the Singapore Companies Act. It becomes mandatory to make annual filings with the Accounting and Corporate Regulatory Authority, the Inland Revenue Authority of Singapore (IRAS) and other related Authorities. Company Compliance is crucial for meeting these statutory obligations.

The company secretary must be residing locally in Singapore and he/she must not be the sole director of the company.

The secretary of a public company must comply with section 171(1AA) of the Companies Act i.e. must possess at least one of the following qualifications:

Been a secretary of a company for at least 3 of the 5 years immediately before his appointment as secretary of the public company.

- Qualified person under the Legal Profession Act (Cap. 161).

- Public accountant registered under the Accountants Act (Cap. 2).

- Member of the Institute of Certified Public Accountants of Singapore.

- Member of the Singapore Association of the Institute of Chartered Secretaries and Administrators.

- Member of the Association of International Accountants (Singapore Branch).

- Member of the Institute of Company Accountants, Singapore.

Statutory Registers of a Singapore Company

The Singapore Companies Act requires every company to maintain certain registers. These statutory registers are a part of the company’s informative records and are usually maintained as official books together with the Constitution of the Company, Share Certificates, Common Seal, all Minuted Resolutions, etc.

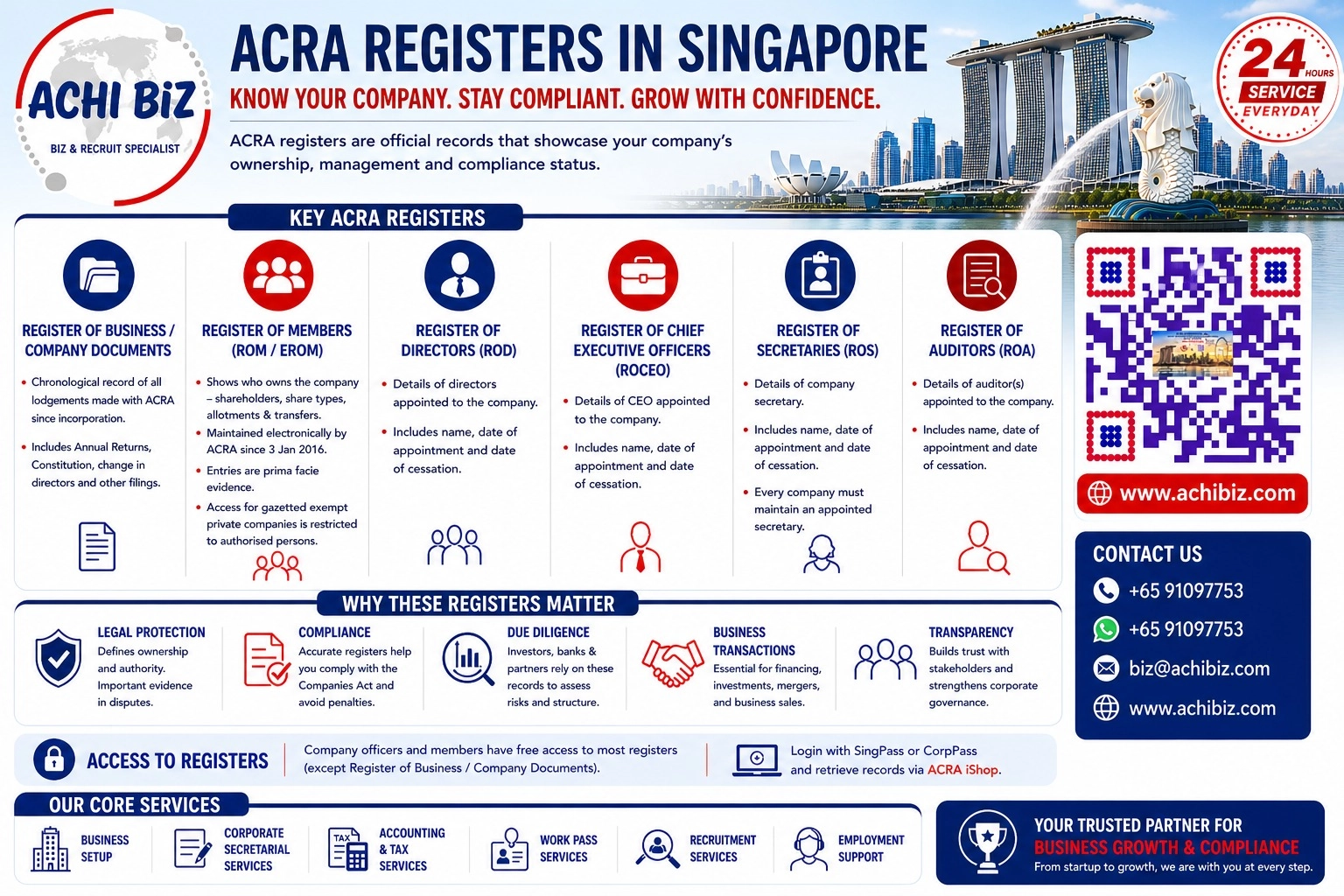

Registers available with ACRA

Registers available with ACRA

However certain registers are available either for purchase for a fee or free from the regulatory authority ACRA with effect from 03-Jan-2016.

What Are ACRA Registers?

ACRA registers Singapore are official records maintained either by the company or electronically by ACRA. They give a clear picture of who owns the company, who manages it, who is responsible for compliance, and what filings have been made over time. These records are essential for Singapore company transparency requirements and are often reviewed by banks, investors, auditors, and regulators.

Following is the list of available registers from ACRA:

|

Name of Registers

|

Details of Registers

|

|

|---|---|---|

|

Register of Business / Company Documents

|

|

|

|

Register of Members (ROM)

|

|

|

|

Register of Directors (ROD)

|

|

|

|

Register of Chief Executive Officers (ROCEO)

|

|

|

|

Register of Secretaries (ROS)

|

|

|

|

Register of Auditors (ROA)

|

|

|

|

Note:

|

||

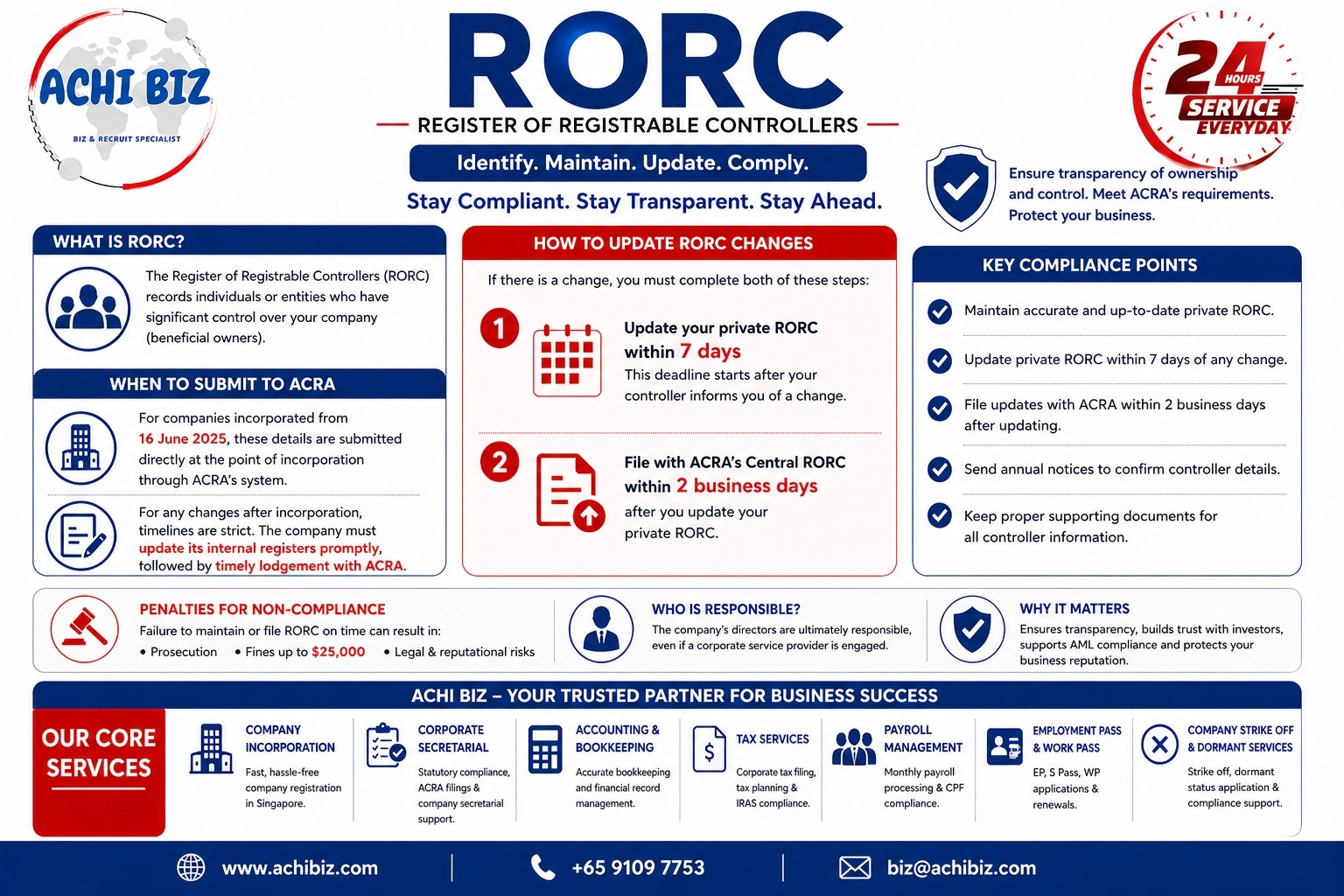

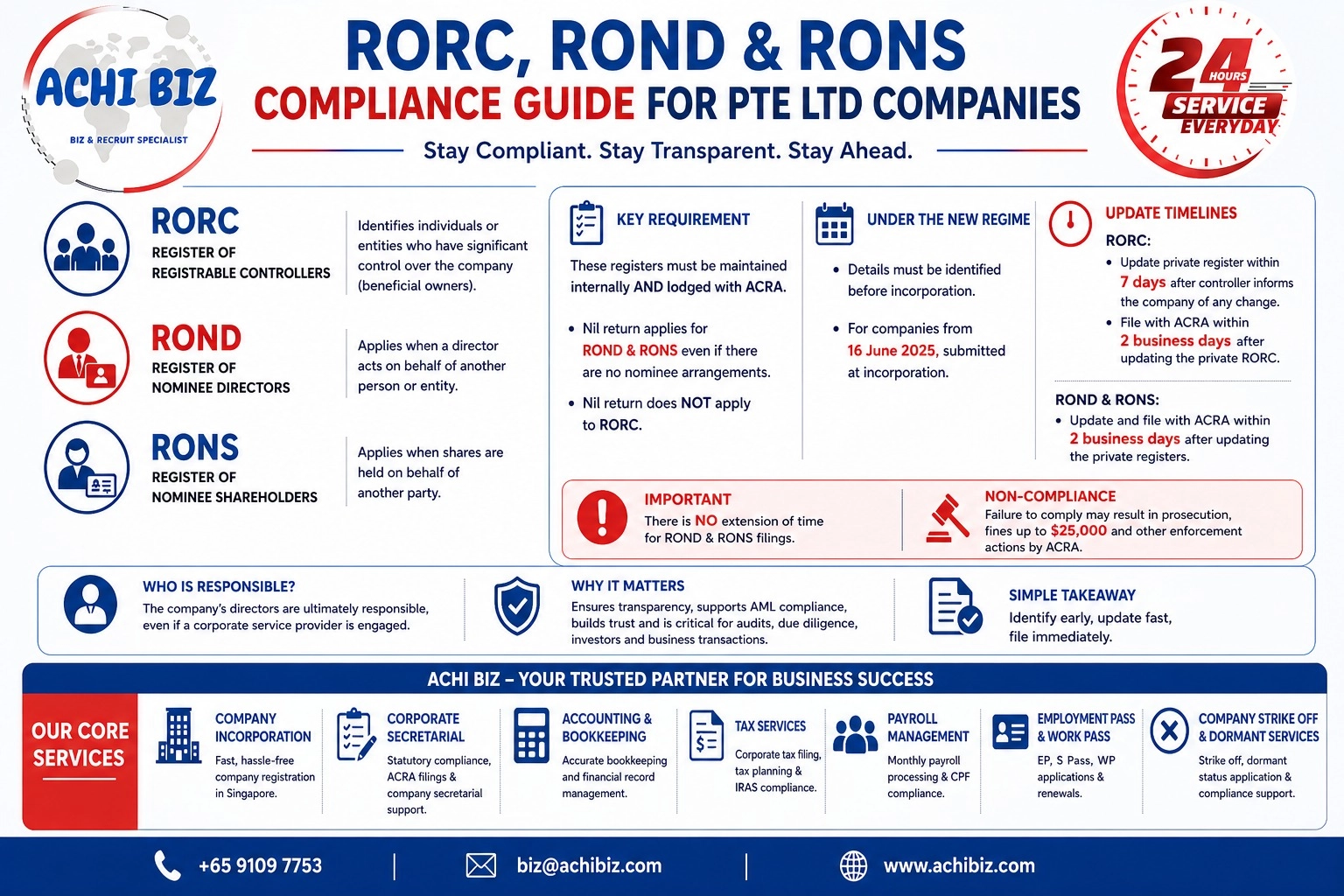

Register of Registrable Controllers

Requirement for Companies, Foreign Companies and Limited Liability Partnerships to maintain Register of Registrable Controllers.

With effect from 31 March 2017, companies, foreign companies and LLPs (unless exempted) will be required to maintain beneficial ownership information in the form of a register of registrable controllers, and to make the information available to public agencies upon request.

The aim is to make the ownership and control of corporate entities more transparent and reduce opportunities for the misuse of corporate entities for illicit purposes. This will bring Singapore in line with international standards, and boost Singapore’s on-going efforts to maintain our strong reputation as a trusted and clean financial hub.

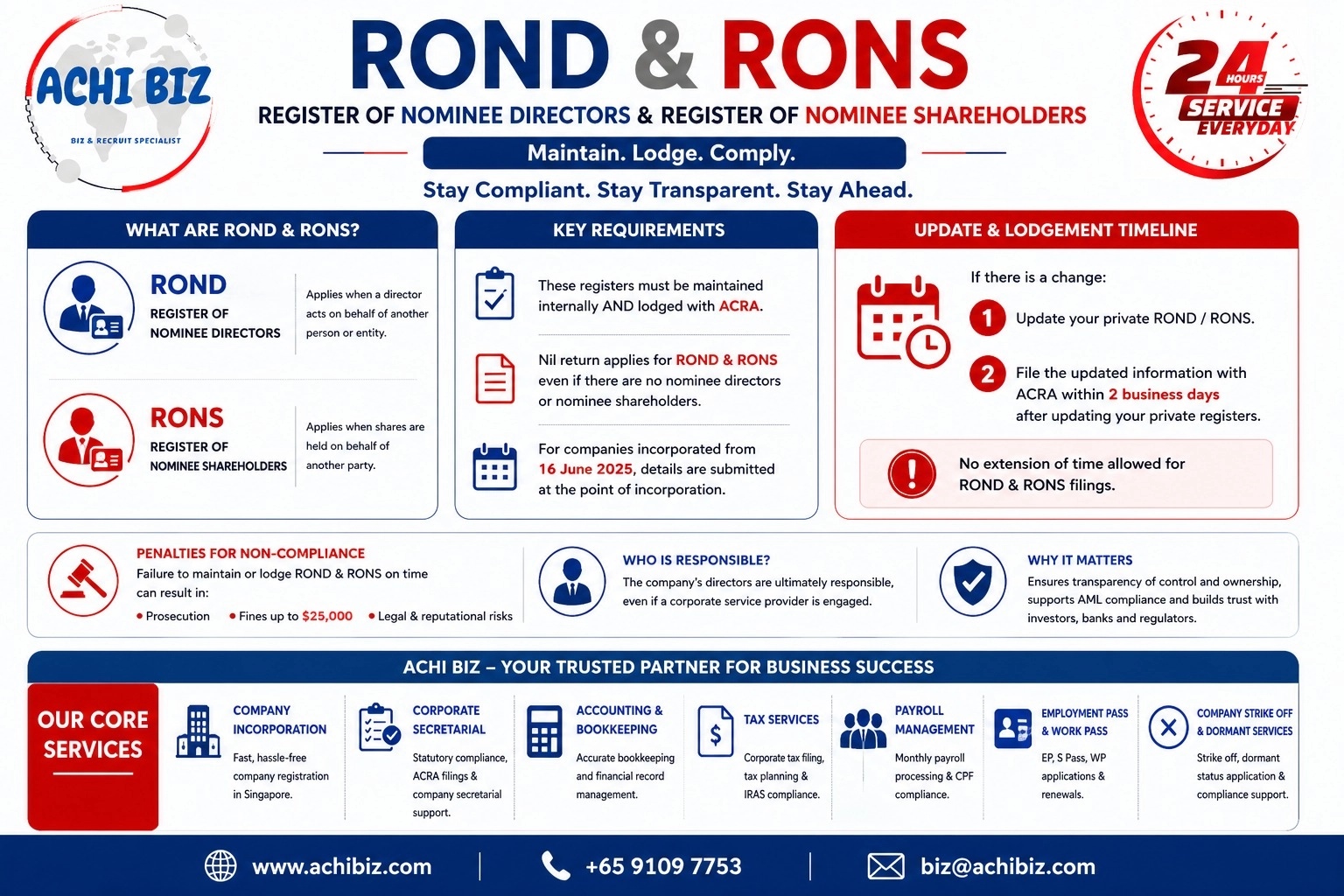

Register of Nominee Directors (ROND) & Nominee Shareholders (RONS)

Register of Nominee Directors

Register of Nominee Directors

With effect from 31 March 2017, Companies are required to each:

- keep a register of its nominee directors containing the particulars of the nominators of the company’s nominee directors; and

- produce the register of nominee directors and any related document to the Registrar, an officer of the Accounting and Corporate Regulatory Authority or a public agency, upon request.

Unlike the register of controllers for companies, companies are not required to take reasonable steps (including sending out notices) to identify their nominee directors, or to update or correct inaccuracies in the particulars contained in their registers of nominee directors.

Instead, nominee directors are required to inform their respective companies of the fact that they are nominees and provide the prescribed particulars of their nominators to their companies within the applicable timelines.

Register of Nominee Shareholders (RONS)

Captures situations where shares are held on behalf of another person, including:

- Nominee shareholder details

- Beneficial owner information

👉 Ensures transparency in share ownership structures.

⚠️ Must also be maintained and updated with ACRA.

ACRA Central Register Requirements (RORC, ROND & RONS)

ACRA Central Register Requirements (RORC, ROND & RONS)

In addition to maintaining internal registers, Singapore requires certain registers to be lodged or updated with ACRA’s central register system.

These include:

- Register of Registrable Controllers (RORC)

- Register of Nominee Directors (ROND)

- Register of Nominee Shareholders (RONS)

👉 Companies must ensure that these registers are:

- Properly maintained internally

- Timely updated in ACRA’s central registry

⚠️ Failure to comply can result in penalties of up to $25,000.

This is a serious enforcement area, and ACRA takes it strictly.

Frequently Asked Questions (FAQs) – RORC, ROND & RONS in Singapore

❓ What is RORC in Singapore?

👉 The Register of Registrable Controllers (RORC) records individuals or entities with significant control over a company, also known as beneficial owners.

❓ What is ROND in Singapore?

👉 The Register of Nominee Directors (ROND) records directors who act on behalf of another person or entity, including details of the nominator.

❓ What is RONS in Singapore?

👉 The Register of Nominee Shareholders (RONS) captures situations where shares are held on behalf of another party, identifying the beneficial owner.

❓ Are RORC, ROND and RONS mandatory in Singapore?

👉 Yes, all Singapore Pte Ltd companies must maintain these registers as part of statutory compliance under the Companies Act.

❓ Do RORC, ROND and RONS need to be filed with ACRA?

👉 Yes, these registers must be maintained internally and also lodged with ACRA’s central register system.

❓ When must RORC, ROND and RONS be submitted to ACRA?

👉 For companies incorporated from 16 June 2025, these details are submitted at the point of incorporation. For any changes, updates must be lodged within 2 business days after updating the private registers.

❓ What is the timeline to update RORC?

👉 The private RORC must be updated within 7 days after the controller informs the company of any change, and the update must be filed with ACRA within 2 business days after that.

❓ Do I need to file ROND and RONS if there are no nominee arrangements?

👉 Yes, a nil return must still be lodged for ROND and RONS even if there are no nominee directors or nominee shareholders.

❓ Does nil return apply to RORC?

👉 No, the nil concept applies specifically to ROND and RONS, but companies must still properly maintain and assess their RORC.

❓ Can I apply for an extension of time for ROND and RONS filing?

👉 No, extensions are not allowed. Late filing may result in prosecution and penalties.

❓ What are the penalties for non-compliance?

👉 Failure to comply may result in fines of up to $25,000, enforcement actions by ACRA, and potential legal consequences for directors.

❓ Who is responsible for maintaining these registers?

👉 The company’s directors are ultimately responsible, even if a corporate service provider is engaged.

❓ Why are RORC, ROND and RONS important?

👉 They ensure transparency in ownership and control, support regulatory compliance, and are essential for audits, due diligence, and investor confidence.

❓ How can Achibiz help with RORC, ROND and RONS Compliance?

👉 Achibiz provides end-to-end corporate secretarial services, including maintaining statutory registers, handling ACRA lodgements, ensuring compliance timelines, and supporting companies from incorporation to strike-off.

Filing Requirements for Register of Controllers (RORC) (W.e.f: 30-July 2020)

As part of ongoing efforts to uphold Singapore’s reputation as a trusted financial hub, and in line with international practices, ACRA has implemented a new requirement for all companies, foreign companies and Limited Liability Partnerships (LLP), unless exempted, to lodge information on their Registers of Registrable Controllers (RORC) with ACRA via BizFile+ from 30-July 2020. This is in addition to the existing requirements for companies and LLPs to maintain a RORC at the registered office address.

The RORC information lodged with ACRA will be accessible to public agencies in Singapore such as law enforcement agencies. Members of the public will not be able to access the RORC information or purchase any extracts of these lodgements.

Companies, foreign companies and LLPs are required to continue to maintain a RORC at the registered office address, and update any changes to the RORC information prior to updating the same information with ACRA within two business days. Alternatively, a Registered Filing Agent (RFA) may be engaged to lodge the RORC information with ACRA on behalf of the entity.

Timeline and Requirement Under the New ACRA Regime

Under the current ACRA framework, RORC, ROND, and RONS must be identified even before incorporation to ensure transparency from the start.

For companies incorporated from 16 June 2025, these details are submitted directly at the point of incorporation through ACRA’s system.

Who can lodge RORC information on behalf of business entities?

Only authorised position holders of the business entity (e.g. directors and secretaries of company / partners of LLPS) as well as RFAs that have been authorised by the business entity can lodge RORC information in BizFile+.

RFAs Lodging RORC information on behalf of their clients

RFAs can only perform transactions, including lodging of RORC information, for entities which are in the client list submitted to ACRA. RFAs must ensure that they have been authorised by their clients to lodge and update the RORC information on their behalf.

Is there a need to update information of past controllers whom have already ceased to be controllers of the entity?

Particulars of previous controllers should also be uploaded with ACRA as previously identified. The date which they ceased to be controllers should also be updated accordingly.

Is there any penalty for late lodgement?

There is no penalty for late lodgement for this transaction. However, entities that are found to have failed to lodge RORC information with ACRA within the deadline, may face enforcement action with a fine up to $5,000 upon conviction.

What are the penalties for failing to lodge RORC with ACRA?

The companies/LLPs will be guilty of an offence, and shall be liable upon conviction, to a fine not exceeding $5,000.

Commencement Of New Requirements Of The Corporate Registers (Miscellaneous Amendments) Act

1) To strengthen Singapore’s corporate governance regime, and reaffirm Singapore’s commitment to combating laundering, terrorism financing and other threats to the integrity of the international financial system, the Accounting and Corporate Regulatory Authority (ACRA) has introduced a new requirement for companies, including foreign companies, and Limited Liability Partnerships (LLPs).

Maintaining Registers of Nominee Shareholders (RONS)

2) Companies, including foreign companies, are required to maintain a Register of Nominee Shareholders (RONS) at their registered office or at the registered office of their appointed Registered Filing Agent. The RONS will need to contain prescribed particulars of the nominator(s) of the company’s nominee shareholder(s). Companies and foreign companies must set up their RONS by 5 December 2022.

3) To assist Company Compliance in the setting up and maintenance of the RONS, ACRA has developed and published a new guidance document for the RONS.

Identification of Registrable Controllers

4) Companies and LLPs who had previously been unable to identify a registrable controller who has a significant interest in or significant control over them will now be required to identify individuals with executive control over them as their registrable controller(s).

- For Company Compliance, this would be each director with executive control and each Chief Executive Officer.

- For LLPs, this would be each partner with executive control.

You may also refer to the updated Register of Registrable Controllers’ Guidance[1] for more information.

5) Registered Filing Agents (RFAs) who have been appointed by their customers to maintain their RORCs are encouraged to remind their customer(s) of this new requirement and to update their RORC by 5 December 2022.

Failure to update the RORC may lead to prosecution and a fine of up to $25,000.

Lodging RORC information with ACRA

6) The steps to be taken for the lodgment of updated RORC information with ACRA are set out below:

- a) Log in to BizFile+ portal.

- b) Click on “e-Services” > “Others” > “Update Register of Registrable Controllers”.

- c) Select “No controllers identified” and complete the new section by updating the particulars of the individual(s) with executive control before submitting the information.

Financial Year End (FYE)

Every Singapore Company must plan its Financial Year End (FYE) that represents the completion of its accounting period. It is not necessary that the FYE of a Company matches with the regular annual calendar. It could fall on any day of the year.

The fiscal year of a Company is taken as the financial year. It is up to the Company to decide its FYE, and most Singapore Companies assign 31st December, 31st March, 30th June or 30th September as the ending date of their fiscal year.

It is in the best interests of a Singapore Company to fix their FYE within 365 days. This helps the Company to take advantage of the partial Tax Exemption offered for new start-ups. The Singapore Law offers partial exemption to both new start-ups and older entities.

Requirements for companies in preparing, auditing and filing of financial statements

Please refer to the table below to determine if a company needs to prepare, audit and file financial statements with their Annual Return submission.

Key changes to Companies Act relating to Audit and Preparation of Financial Statements

|

Topic

|

Current Provision/Requirement

|

Changes and Reasons

|

|---|---|---|

|

Audit exemption for small companies

[New section 205C and Thirteenth Schedule]

|

An exempt private company with annual revenue of $5m or less for the financial year is exempt from auditing its financial statements.

An exempt private company is a company which has not more than 20 members and in which no corporation holds any beneficial interest in its shares. |

A “small company” is exempt from auditing their financial statements. A company qualifies as a small company if:

(a) it is a private company in the financial year in question; and (b) it meets at least 2 of 3 following criteria for immediate past two financial years:

For a company which is part of a group: (a) the company must qualify as a small company; and (b) entire group must be a “small group” to qualify to the audit exemption. For a group to be a small group, it must meet at least 2 of the 3 quantitative criteria on a consolidated basis for the immediate past two consecutive financial years. Where a company has qualified as a small company, it continues to be a small company for subsequent financial years until it is disqualified. A small company is disqualified if: (a) it ceases to be a private company at any time during a financial year; or (b) it does not meet at least 2 of the 3 the quantitative criteria for the immediate past two consecutive financial years. Where a group has qualified as a small group, it continues to be a small group for subsequent financial years until it does not meet at least 2 of the 3 the quantitative criteria for the immediate past two consecutive financial years. Reasons for amendment by ACRA

|

|

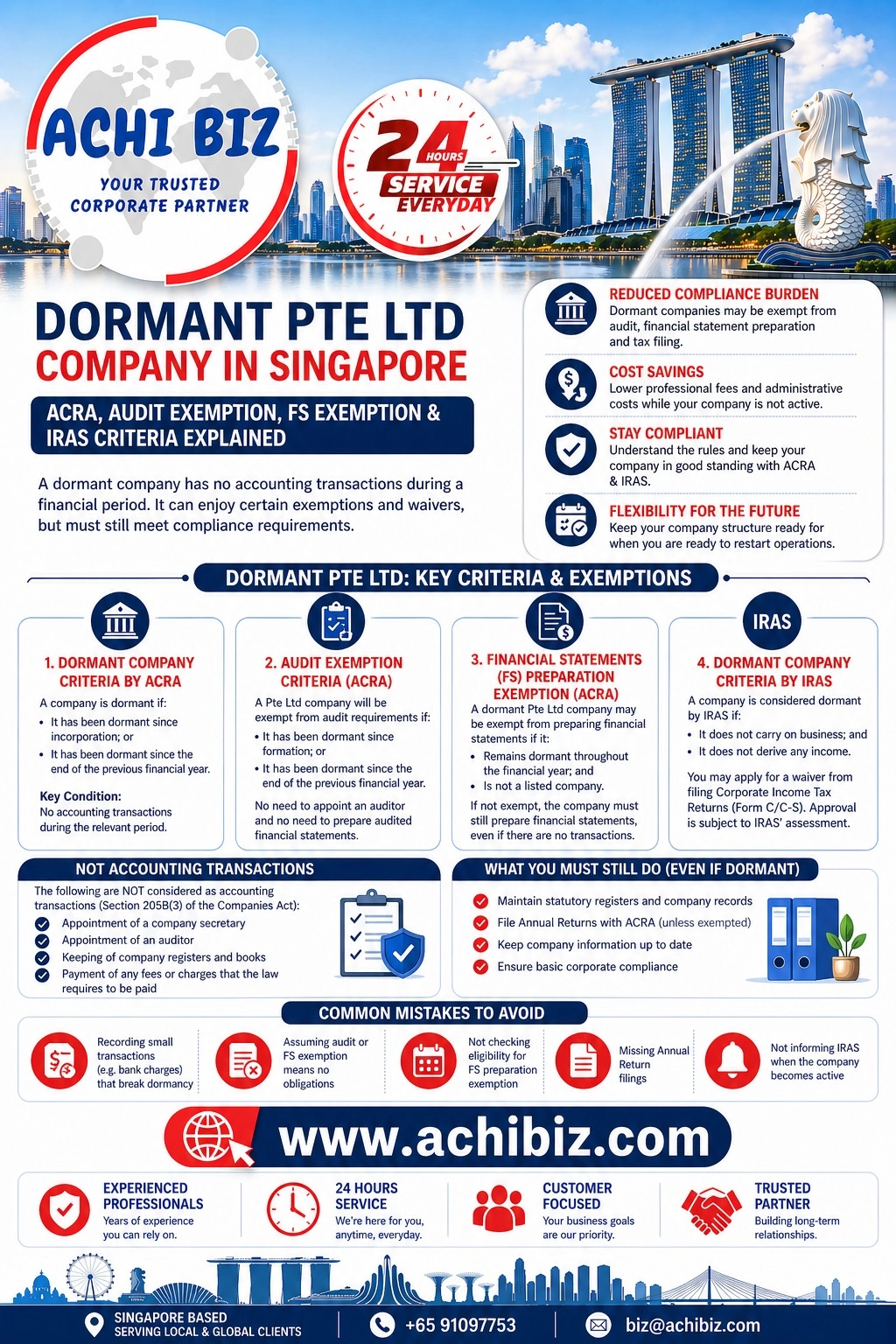

Exemption from preparation of financial statements for dormant unlisted companies

[New section 201A] |

A dormant company is exempted from the statutory audit requirements but is still required to prepare financial statements.

|

A dormant non-listed company (other than a subsidiary of a listed company) is exempt from requirement to prepare financial statements, if:

(a) the company fulfils the substantial assets test; and (b) the company has been dormant from the time of formation or since the end of the previous financial year. The substantial assets test is that the total assets of the company at any time within the financial year must not exceed $500,000. For a parent company, the consolidated total assets of group at any time within the financial year must not exceed $500,000. Dormant listed companies and their subsidiaries, and dormant unlisted companies which do not fulfil the substantial asset test must prepare financial statements but are exempt from audit. This remains unchanged from the current position. Reasons for amendment by ACRA The new exemption from preparation reduces regulatory costs for dormant companies which have lower public impact. |

|

Resignation of auditor before end of term of office

[New sections 205AA to 205AF] |

An auditor can resign if he is not the sole auditor, or at a general meeting, and where a replacement auditor is appointed.

|

An auditor of a non-public interest company (other than a subsidiary of a public interest company) may resign before the end of the term of his appointment by giving written notice to the company.

An auditor of a public interest company or a subsidiary of a public interest company may resign before the end of the term of his appointment by giving written notice to the company, and upon consent by the Registrar of Companies. The auditor must give the company reasons for his resignation, and any such reasons must be circulated by the company to the shareholders, unless the Court orders otherwise. A public interest company will be defined to include a company listed or to be listed on a securities exchange in Singapore or such other company as the Minister for Finance may prescribe. Additional categories of companies are intended to be prescribed to align the definition with similar concepts for the purposes of the Practice Monitoring Programme conducted by ACRA under the Accountants Act. Reasons for amendment by ACRA The changes allow auditors to resign mid-term, especially in situations where the company refuses to hold a general meeting to appoint a replacement auditor. The requirement for Registrar’s consent will allow the Registrar to stop the resignation in the public interest where necessary. The reasons for resignation for companies with greater public interest should be circulated so as to promote greater corporate governance. |

|

Framework for revision of defective financial statements

[New section 202A and 202B] |

Currently there is no express framework for revision of defective financial statements.

|

A new regulatory framework is introduced to allow directors of a company to revise defective financial statements, where the financial statements do not comply with the Companies Act (including compliance with the financial reporting standards). Consequential revisions may also be made to the summary financial statement or the directors’ statement.

The Registrar of Companies may apply to Court for a declaration that the financial statements of a company do not comply with the Companies Act (including compliance with the financial reporting standards), and an order to require the directors of a company to cause the financial statements to be revised. Reasons for amendment

|

Who Needs to File Financial Statements (FS) with their Annual Return (AR) submission.?

All Singapore (SG) incorporated companies are required to file financial statements (FS) with ACRA, except for those which are exempted. Some companies will file a full set of FS in XBRL format, while some others will file key financial data in XBRL format and a full set of signed copy of the FS tabled at annual general meeting and/or circulated to members (AGM FS) in PDF. If you own a sole proprietorship, partnership, limited liability partnership, or limited partnership, you are not required to file FS with ACRA.

To file FS in XBRL format, please upload your XBRL file to BizFinx server (e.g. through BizFinx preparation tool), then proceed to file it as part of Annual Return in BizFile+. More information on how to upload your XBRL file.

Revised XBRL filing requirements

ACRA has revised the filing requirements and data elements in XBRL format for companies. This is a part of our efforts to streamline the filing of FS.

The effective implementation date for companies to file FS in XBRL format using the revised filing requirements and data elements are as follows:

- Companies are required to apply the revised filing requirements and data elements on or after 1 May 2021;

- Companies can opt to voluntarily apply the revised filing requirements and data elements from 16 May 2020 to 30 April 2021 (both dates inclusive).

What are the Types of XBRL to be used for Entities in Singapore?

There are four templates to be used by companies to meet the revised filing requirements and data elements:

|

#

|

Template of XBR

|

Data Elements

|

|---|---|---|

|

1

|

Full XBRL

|

The number of data elements for this template has been reduced by 50% to about 210 data elements. It will capture the information in primary statements and selected notes to FS.

|

|

2

|

Simplified XBRL

|

This template, which replaces XBRL FSH (General), has about 120 data elements. It will capture the complete information in the statements of financial performance and position.

|

|

3

|

XBRL FSH (Banks)

|

There is minimal change to this template. This template has about 80 data elements.

|

|

4

|

XBRL FSH (Insurance)

|

There is minimal change to this template. This template has about 80 data elements.

|

The table below summarises the revisions to the filing requirements and data elements:

|

Company type

|

Company type What you need to file

|

||

|---|---|---|---|

|

|

||

|

|

||

|

|

||

|

|

||

|

|

||

Definition of smaller company

A smaller company mentioned in the table above refers to a company whose revenue and total assets for the current financial year do not exceed S$500,000, respectively. The assessment of revenue and total assets should be made based on the FS that are required to be prepared under the Companies Act. When the company controls, jointly controls or has significant influence over other entities, its revenue and total assets should be assessed based on consolidated figures, unless the company is exempted by the accounting standards or by ACRA from preparing consolidated FS.

The amount thresholds of S$500,000 are to be determined based on the FS, regardless of the number of months in the financial year covered by the FS. For FS presented in foreign currency, revenue should be translated based on average rates over the financial year and total assets to be translated based on closing rate as of financial year-end.

Definition of non-publicly accountable company

A non-publicly accountable company mentioned in the table above refers to a company that is not:

a) a company that is listed or is in the process of issuing debt or equity instruments for trading on a securities exchange in Singapore;

b) a company whose securities are listed on an exchange outside Singapore;

c) one of the following financial institutions:

· entity that is part of the banking and payment systems (namely, licensed banks1, financial institutions approved under section 28 of the Monetary Authority of Singapore Act (Chapter 186), operators of payment systems designated under section 42 of the Payment Services Act 2019 (Act 2 of 2019), settlement institutions of payment systems designated under section 42 of the Payment Services Act 2019, persons that have in force a standard payment institution licence granted under section 6 of the Payment Services Act 2019, persons that have in force a major payment institution licence granted or deemed to have been granted under section 6 of the Payment Services Act 2019 and licensed finance companies);

- licensed insurer, foreign insurer under Lloyd’s Asia Scheme and registered insurance broker;

- capital market infrastructure provider (namely, approved holding companies, approved exchanges, recognised market operators, approved clearing houses and recognised clearing houses under the Securities and Futures Act (Chapter 289));

- capital markets intermediary (namely, holders of capital market services licence, licensed financial advisers, registered fund management companies, licensed trust companies and approved trustee for collective investment scheme);

- licensed trade repository, authorised and exempt benchmark administrator under the Securities and Futures Act (Chapter 289);

- operator of the Central Depository System under the Securities and Futures Act (Chapter 289);

- trustee-manager of listed registered business trust;

- designated financial holding company under the Financial Holding Companies Act2; and

- licensed credit bureau under the Credit Bureau Act2.

1 “Licensed banks” should be read as “banks or merchant banks licensed under the Banking Act (Chapter 19)” when section 24 of the Banking (Amendment) Act 2020 relating to merchant banks come into force.”

2 Applicable once the Acts commences.

Definition of solvent exempt private company

A private company can have not more than 50 members. An exempt private company can be a private company with less than 20 members, and does not have any corporations holding beneficial interest in its shares (whether directly or indirectly). An exempt private company can also be a private company owned by the Government that is declared in the Gazette to be an exempt private company.

- An exempt private company is insolvent if it is unable to meet its debts when they are due. Insolvent EPCs are required to file FS as mentioned above.

- Solvent EPCs only need to make an online declaration of their solvency, and filing FS is voluntary.

Statutory Returns

The Company Secretary will update the ACRA on the following:

- Changes in the particulars of the Directors(s) or when the Directors(s) are changed

- Changes in the name or address of the Director(s)

- Removal of Company Officers anyone from office according to the constitution of the Singapore Companies Act

- Disqualification of Directors

- Appointments, Resignations or Deaths of Company Officers

- Change in Company’s name

- Annual Returns

- Change, revocation or adoption of Company constitution

- Issuance of Shares

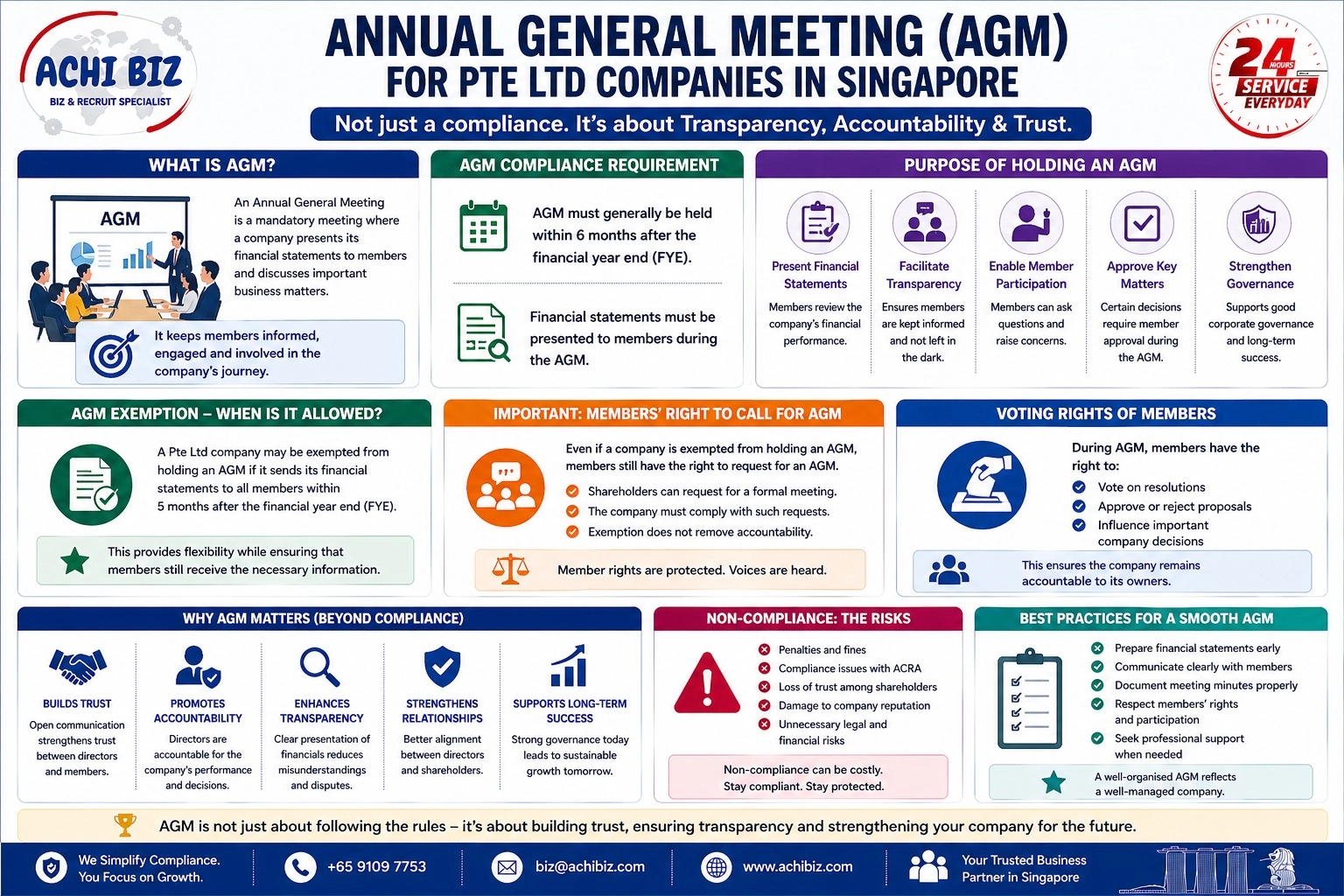

Annual General Meeting (AGM)

An AGM is a mandatory annual meeting of shareholders. At the AGM, your company will present its Financial Statements (also known as “Accounts”) before the shareholders (also known as “Members”) so that they can raise any queries regarding the financial position of the company.

Timeline for Holding AGM

|

For Companies with FYE ending before 31 Aug 2018

|

For Companies with FYE ending on or after 31 Aug 2018

|

|

|---|---|---|

|

(a) Timeline 1: Hold first AGM within 18 months of incorporation, and subsequent AGMs yearly at intervals of not more than 15 months

(b) Timeline 2: Financial statements tabled at AGM must be made up to a date within 4 months (for listed company) or 6 months (for any other company) before the AGM date. |

For listed companies:

Hold AGM within 4 months after FYE |

|

|

For listed companies:

Hold AGM within 4 months after FYE |

||

Click here to learn more about Annual General Meeting (AGM)

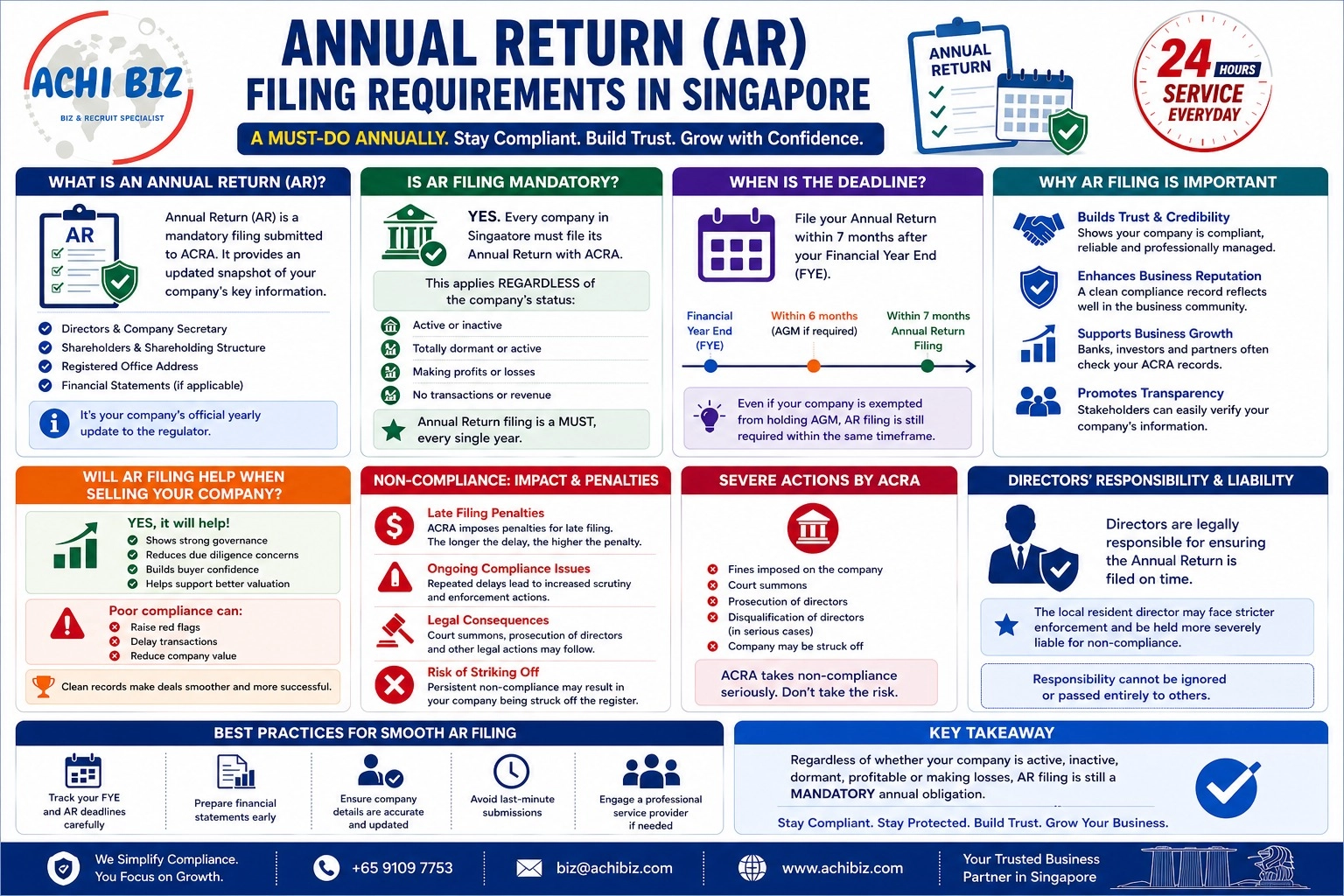

Requirements for filing Annual Returns (ARs)

Requirements for filing Annual Returns (ARs)

All locally-incorporated companies are required to file Annual Returns. The appointed officer of the company e.g. director or company secretary may file the Annual Returns online via BizFile+. Alternatively, the company can engage the services of a registered filing agent like ACHI to file the Annual Return on behalf of the company.

In addition, as part of the annual obligations, companies and directors are required to prepare and present a true and fair view of the company’s financial statements to their shareholders.

When does a company need to file Annual Return?

For companies with financial year-end (FYE) ending on or after 31 Aug 2018, the timelines for holding Annual General Meetings (AGMs) and the filing of annual returns are aligned with the company’s FYE. This is to provide greater clarity in the computation of timelines and facilitate ease of compliance.

Every company in Singapore must file its Annual Return in its appropriate due date with the Company Registrar otherwise this will incur penalties.

Timeline for filing of Annual Returns (AR)

|

For Companies with FYE ending before 31 Aug 2018

|

For Companies with FYE ending on or after 31 Aug 2018

|

|

|---|---|---|

|

For companies having a share capital and keeping a branch register outside Singapore:

File annual returns within 60 days after AGM |

For companies having a share capital and keeping a branch register outside Singapore:

File annual returns within 6 months (if listed) or 8 months (if not listed) after FYE |

|

|

For other companies

File annual returns within 30 days after AGM |

For other companies:

File annual returns within 5 months (if listed) or 7 months (if not listed) after FYE Annual return can be filed only:

|

|

|

To prevent companies from arbitrarily changing their FYE, the following safeguards are put in place by ACRA:

|

||

|

A company’s financial periods starting on or after 31 Aug 2018 by default will be taken to be a period of 12 months for each financial period.

|

||

|

Important information for companies with unusual financial year period:

|

||

|

Important information for newly Incorporated companies that have yet to file Annual Returns:

|

||

Filing of Financial Statements (FS) with Annual Returns

(i) Companies required to file financial statements with their Annual Return

- Financial Statements are to be filed in XBRL format.

(ii) Companies not required to file their financial statements with their Annual Return

Companies that are not required to file financial statements must instead submit a declaration online when they file their Annual Returns via BizFile+. The declaration will appear in the transaction based on the company type selected during annual return filing in BizFile+ .

Who Needs to File Financial Statements (FS)?

All Singapore incorporated companies are required to file financial statements with ACRA, except for those which are exempted. Some companies will file a full set of financial statements in XBRL format, while some others will file only salient financial data in XBRL format and a full set of financial statements in PDF. The filing requirements depend on the type of company you own (see table below).

If you own a sole proprietorship, partnership, or limited partnership, you are not required to file financial statements with ACRA.

|

Type of company

|

Financial Statements you need to file

|

|

|---|---|---|

|

Public / private companies (limited or unlimited by shares), except those under (a) and (b) below

|

Full set of financial statements in XBRL format.

|

|

|

(a) Specific companies regulated by MAS, such as commercial banks, merchant banks, insurance companies, and finance companies*

*Companies other than the specified types (e.g. money changers) are required to file a full set of XBRL financial statements |

Financial Statements Highlights in XBRL format, plus PDF copy of the financial statements.

|

|

|

(b) Companies permitted to use accounting standards other than SFRS, SFRS for Small Entities, and IFRS**

** SFRS stands for Singapore Financial Reporting Standards and IFRS stands for International Financial Reporting Standards |

Financial Statements Highlights in XBRL format, plus PDF copy of the financial statements.

|

|

|

Solvent Exempt Private Companies (EPCs)

|

Exempted from filing financial statements. Nonetheless, you are encouraged to file the full set of financial statements or the financial statement highlights in XBRL format.

|

|

|

Insolvent EPCs

|

You must either:

|

|

|

Companies limited by guarantee

|

PDF copy of the financial statements

|

|

|

Foreign companies, or local branches of foreign companies

|

PDF copy of the financial statements

|

|

Differences between a solvent and insolvent EPC

A private company can have not more than 50 members. An exempt private company (EPC) can be a private company with less than 20 members, and does not have any corporations holding beneficial interest in its shares (whether directly or indirectly). An EPC can also be a private company owned by the Government that is declared in the Gazette to be an EPC.

- An EPC is insolvent if it is unable to meet its debts when they are due. Insolvent EPCs are required to file financial statements as mentioned above.

- Solvent EPCs only need to make an online declaration of their solvency, and filing financial statements are voluntary.

Prepare Financial Statements Highlights

Not all companies are required to file a full set of financial statements in XBRL format. Some companies are only required to file financial statements highlights in XBRL format, with a PDF of the financial statements tabled at the AGM. Refer to the above Table whether your company is eligible only to file financial statements highlights in XBRL format.

Applying for Exemptions from XBRL Filing Requirements

Companies may apply for exemption from XBRL filing requirements from ACRA, for the following:

- Exemptions from specific business rules in filing your financial statements in XBRL format (e.g. removing the requirement for comparative periods in your financial statement, given valid reasons).

- Exemption from filing full set of XBRL financial statements, and instead filing Financial Statement Highlights (FSH) in XBRL format only, if you have valid proof that the full set of XBRL financial statements cannot be prepared.

- Allowing you to file PDF copy of financial statements, with valid proof that you cannot file the full set of XBRL financial statements, or FSH.

Exemptions are evaluated on a case-by-case basis by ACRA.

Some Important Frequently Asked Questions on filing of ARs:

Q: What if a company fails to file its Annual Returns?

A: Enforcement actions will be taken against directors and companies for annual returns filing breaches.

Q: What are some of the transactions that would be disregarded in determining whether a company is dormant?

A:

- The appointment of a secretary of the company;

- The appointment of an auditor;

- The maintenance of a registered office;

- The keeping of registers and books under certain sections of the Companies Act;

- The payment of fees or charges payable under any written law;

- The taking of shares in the company by a subscriber to the Constitution in pursuance of an undertaking of his in the Constitution.

For more details, please refer to s205B of the Companies Act.

Q: My company’s financial statements are exempted from audit, but we have chosen to get our financial statements audited. Should we be filing the unaudited or audited financial statements?

A: Companies that are exempted from audit requirements are not required to have their financial statements audited. Instead, they will prepare unaudited financial statements for purposes of AGMs and filing with ACRA. If the company chooses to have the financial statements audited, it will submit the audited financial statements together with the auditor’s report.

Q: If the company has already filed an Annual Return with ACRA, does it still need to file any documents with IRAS?

A: For a dormant company:

- The company must submit its Income Tax Return (Form C) unless it has been granted a waiver from IRAS. The company may apply for a waiver from IRAS by submitting the form ‘Application for a Waiver to Submit Income Tax Return (Form C) by a Dormant Company.

For all other companies:

- The company which has filed Annual Return with ACRA must also file its Income Tax Return (Form C-S / Form C) and the necessary supporting documents (such as financial statements and tax computation) with IRAS annually.

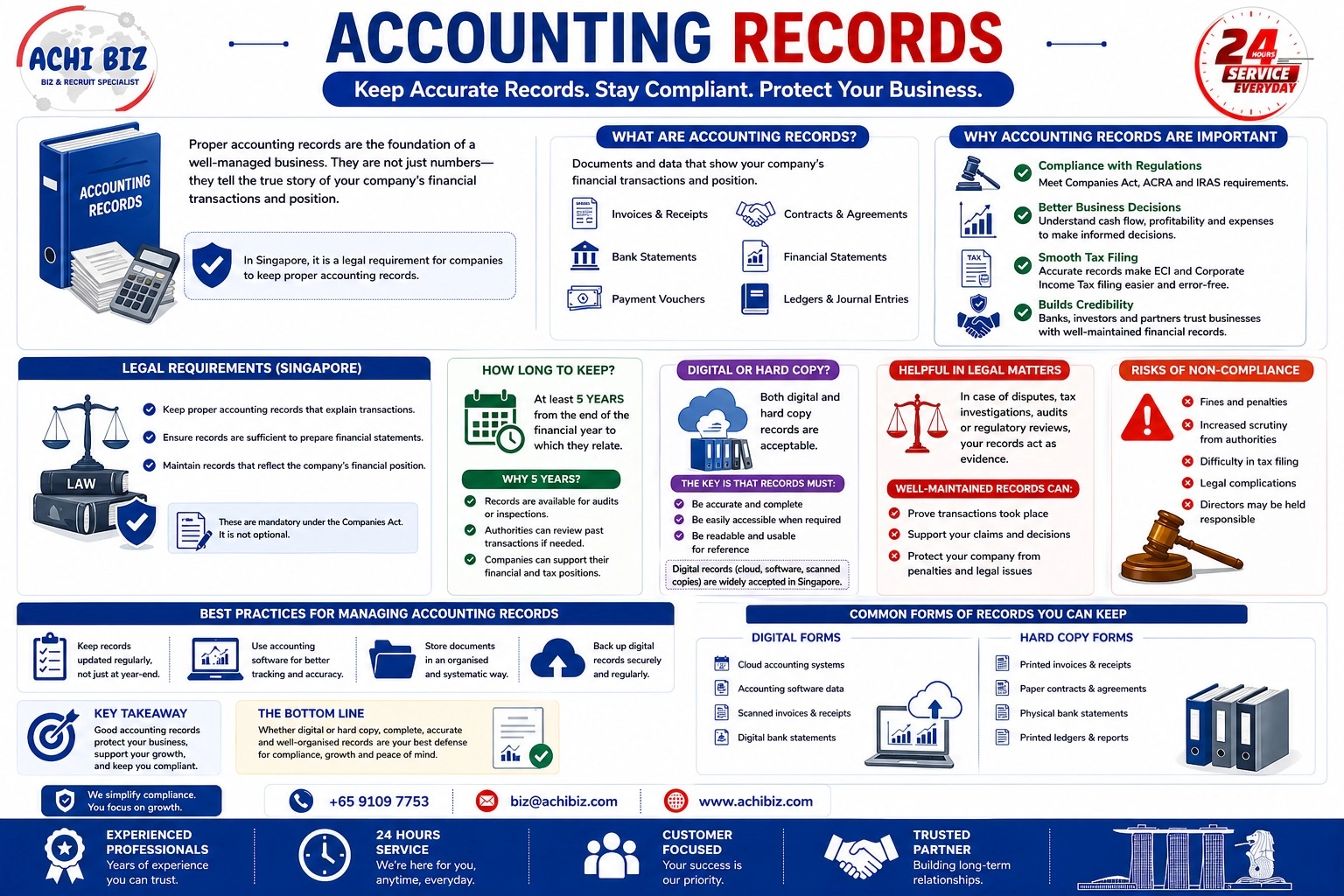

Business Records That Companies Must Keep

Companies are required to keep proper records and accounts of business transactions. Your company must maintain proper records of its financial transactions and retain the source documents, accounting records and schedules, bank statements and any other records of transactions connected with your business.

Using an accounting software helps businesses improve record keeping and comply with tax obligations. Businesses can also use the information captured in the software to ensure that operations are effective and efficient. The IRAS’ Accounting Software Register lists the accounting software that are able to meet IRAS’ technical requirements and businesses considering to use an accounting software for record keeping are encouraged to consider those in this list.

Duration for Records and Accounts Keeping

For accounting records and supporting documents relating to Year of Assessment (YA) 2008 and subsequent YAs, your company must retain the records for a period of five years from the relevant YA. Failure to do so may result in:

- Expenses claimed being disallowed; or/and

- Penalties

Examples:

|

Companies with December financial year end

|

||

|---|---|---|

|

YA

|

Records for period

|

To keep up to

|

|

2014

|

1 Jan 2013 to 31 Dec 2013

|

31 Dec 2018

|

|

2018

|

1 Jan 2017 to 31 Dec 2017

|

31 Dec 2022

|

|

Companies with non-December financial year end, e.g. Jun, Sep

|

||

|---|---|---|

|

YA

|

Records for period

|

To keep up to

|

|

2014

|

1 Oct 2012 to 30 Sep 2013

|

31 Dec 2018

|

|

2018

|

1 Oct 2016 to 30 Sep 2017

|

31 Dec 2022

|

Where a company has been struck off and dissolved, a person who was an officer of the company immediately before the company was dissolved must ensure that all books and papers of the company are retained for a period of at least five years after the date on which the company was dissolved.

Where a company is being wound up, the liquidator of the company must ensure that all the books and papers of the company are retained for a period of at least five years (instead of two years previously) from the date of dissolution of the company.

Guides on Record Keeping

GST-registered Businesses

For companies that are GST-registered, please refer to the Guide “Record Keeping Guide for GST-Registered Businesses” for the record keeping requirements. This will cover requirements for keeping business records in electronic media and imaging systems.

Non-GST-registered Businesses

For companies that are not GST-registered, please refer to the Guide “Record Keeping Guide for Non GST-Registered Businesses” for the record keeping requirements. This will cover requirements for keeping business records in electronic media and imaging systems.

Please refer to the “Record Keeping Checklist”, which provides a summary of the different types of records required.

Appointment of Auditors

Under section 205 of the Companies Act, the directors of a company are required to appoint at least one accounting entity to be the company’s auditor within 3 months of the company’s incorporation. In Singapore, only public accountants or accounting firms approved by the Accounting and Corporate Regulatory Authority (ACRA) can act as company auditors.

Auditors will hold office from the time of their appointment until the conclusion of the company’s next annual general meeting (AGM). Therefore when a newly-incorporated company first appoints an auditor, this auditor will hold office until the conclusion of the company’s first AGM.

Then during the first AGM, the company will have to appoint a new accounting entity (or reappoint the same accounting entity) to act as the company’s auditor until the conclusion of the next AGM. This auditor will then hold office until the conclusion of the company’s subsequent AGM, and so on and so forth.

If the directors fail to appoint a company auditor, any company member may apply to the Registrar to have it appoint an auditor for the company instead.

Exemption from Audit Requirements

Companies that are regarded as a “small company” for a particular financial year, or are dormant, are exempt from audit requirements. These companies therefore do not need to appoint auditors (or have their financial statements audited) for that financial year.

Small Company Exemption

In general, a company will be considered a “small company” if it is a private company throughout the current financial year, and satisfies any 2 of the following criteria for each of the 2 financial years immediately before the current financial year:

- The company’s revenue does not exceed SGD10 million;

- The value of the company’s total assets does not exceed SGD10 million; or

- The company does not have more than 50 employees.

Refer to the Thirteenth Schedule of the CA for the criteria that companies incorporated for less than 3 years, or incorporated before 1 July 2015, have to meet in order to be considered a “small company”.

- For a company which is part of a group:

- (a) the company must qualify as a small company; and

- (b) entire group must be a “small group”

- to qualify to the audit exemption.

- For a group to be a small group, it must meet at least 2 of the 3 quantitative criteria on a consolidated basis for the immediate past two consecutive financial years.

- Where a company has qualified as a small company, it continues to be a small company for subsequent financial years until it is disqualified. A small company is disqualified if:

- (a) it ceases to be a private company at any time during a financial year; or

- (b) it does not meet at least 2 of the 3 the quantitative criteria for the immediate past two consecutive financial years.

- Where a group has qualified as a small group, it continues to be a small group for subsequent financial years until it does not meet at least 2 of the 3 the quantitative criteria for the immediate past two consecutive financial years.

Dormant company

A company will also be exempt from audit requirements if:

- It has been dormant from the time of its formation; or

- It has been dormant since the end of the previous financial year.

A company is dormant during a period in which no accounting transaction occurs. Dormant companies will cease to be considered dormant once such an accounting transaction occurs.

The following are not to be considered as accounting transactions (refer to section 205B(3) of the CA for the full list):

- The appointment of a company secretary

- The appointment of an auditor

- The keeping of company registers and books

- The payment of any fees or charges that the law requires to be paid

What is a solvent exempt private company?

A Solvent exempt private company is a company gazetted as an exempt private company or a private company which no beneficial interest in its shares is held directly or indirectly by any corporation and which has not more than 20 members; and the company confirms that it is able to meet its liabilities as and when they fall due.

Exception to exemption from audit requirements

Even if a company Compliance is exempt from audit requirements, the Registrar may still require the company to lodge its audited financial statements and an auditor’s report if the Registrar is satisfied that the company has breached laws relating to the:

- Keeping of accounting records (section 199 of the CA); or

- Laying of its financial statements at its AGM (section 201 of the CA).

Appointment of Data Protection Officers

Under the Personal Data Protection Act 2012 (PDPA), organisations are required to designate at least one individual as the data protection officer (DPO) to oversee data protection responsibilities and ensure compliance with the PDPA. The DPO function may be a dedicated responsibility or added to an existing role in the organisation. The appointed DPO may also delegate certain responsibilities to other officers.

Responsibilities of the DPO

The responsibilities of a DPO include, but are not limited to:

- Ensuring compliance with PDPA when developing and implementing policies and processes for handling personal data;

- Fostering a data protection culture among employees and communicating personal data protection policies to stakeholders;

- Managing personal data protection-related queries and complaints;

- Alerting management to any risks that might arise with regard to personal data; and

- Liaising with the PDPC on data protection matters, if necessary.

Help Available

Resources

DPOs are encouraged to kick-start the implementation of data protection policies and processes using PDPC’s free-to-use resources such as sample clauses, templates, communication materials and tools available at:

- https://www.pdpc.gov.sg/DP-Professional

Hiring

Organisations may hire a DPO under the Professional Conversion Programme (PCP) for Data Protection Officers scheme which provides skills conversion to train and place professionals, managers, executives and technicians (PMETs) in a DPO role.

Outsourcing of DPO function

Organisations with manpower constraints may outsource operational aspects of the DPO function to a service provider. However, the overall DPO function remains the management’s responsibility.

Data Protection-as-a-Service (DPaaS) is an alternative for organisations to outsource their data protection functions. Organisations may approach any of the listed providers who registered with the Infocomm Media Development Authority (IMDA) to get started on basic data protection practices. For more information, please visit the IMDA website at:

- http://www.imda.gov.sg/dpaas

Organisations Can Now Register Their DPO Information directly at PDPC

Under the Personal Data Protection Act (PDPA), organisations are required to designate at least one individual as the organisation’s DPO, and making the DPO’s business contact information (BCI) publicly available.

Business entities registered with ACRA (including sole-proprietorships, partnerships, limited partnerships, limited liability partnerships and companies) can register and update their DPO’s BCI directly at PDPC.

FAQ on appointment of DPO

Is registration of the DPO with PDPC mandatory?

No, registration of the DPO with PDPC is not mandatory but strongly recommended.

Visit PDPC for more details and FAQs.

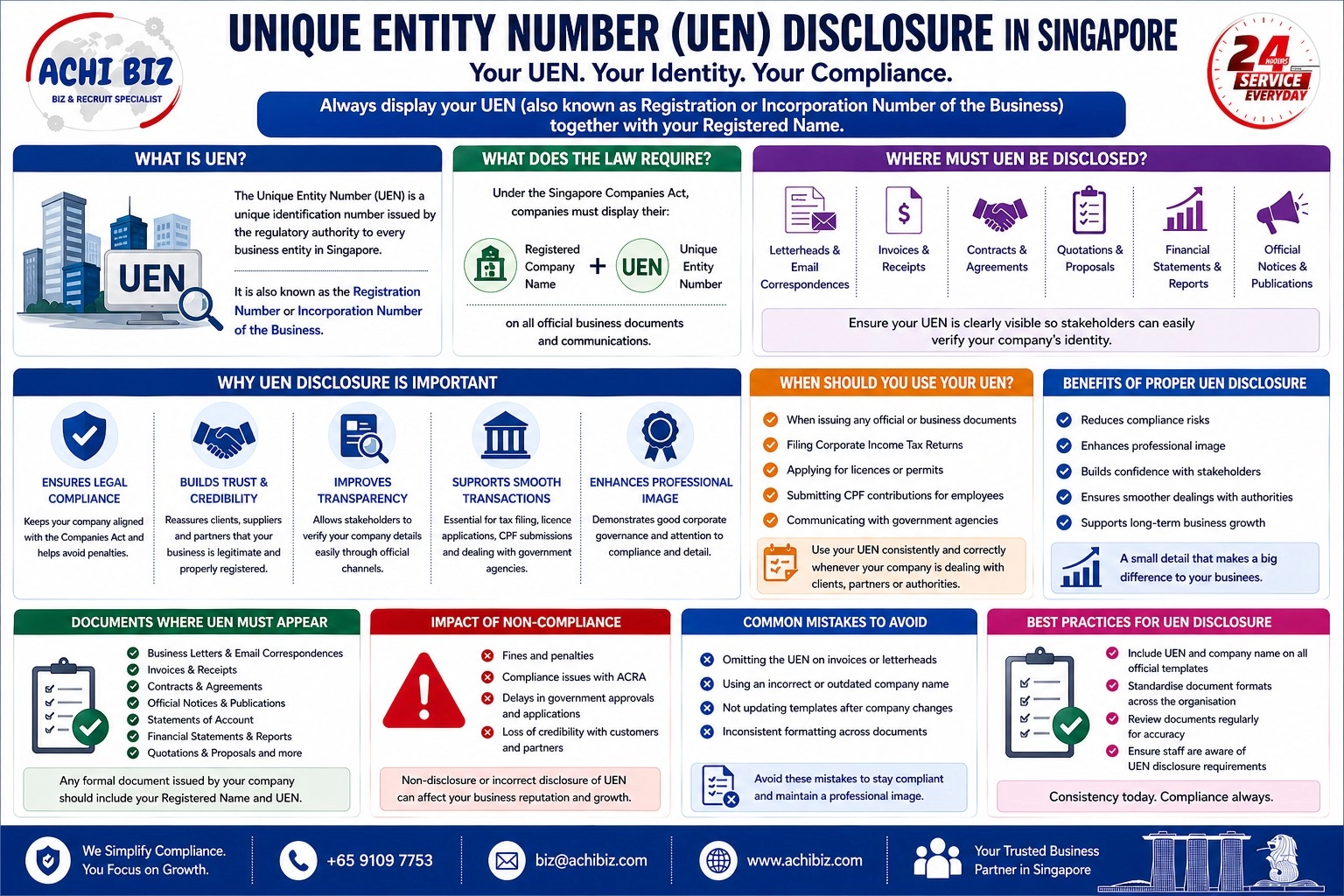

Disclosing of Company Registration Number (UEN)

Unique Entity Number (UEN) Disclosure in Singapore businesses: What You Must Know

If you run a private limited company (Pte Ltd) or any business in Singapore, your Unique Entity Number (UEN) is more than just an identifier—it’s a key part of your business identity.

Also commonly referred to as the registration number or incorporation number of the business, the UEN is used across all official and regulatory matters in Singapore.

Yet, many businesses overlook the importance of UEN disclosure requirements. Failing to display it correctly can lead to compliance issues and even penalties.

, and core services including company incorporation, employment agency services, immigration services, nominee director & shareholder services, accounting & tax services, and corporate secretarial services.](https://achibiz.com/wp-content/uploads/2026/04/ACHI-SA-Image-0091-Keep-Your-Company-Information-Up-To-Date.webp)

Running a Pte Ltd company in Singapore comes with ongoing responsibilities—and one of the most overlooked is keeping your company information and personal particulars of officers up to date.

This includes changes to directors, shareholders, company secretary, registered address, shareholding structure, and personal details such as residential address, passport number, or contact information.

It may sound administrative, but in reality, it’s a core compliance requirement under ACRA. Ignoring it can create serious issues down the line.

What Changes Must Be Updated?

Under Singapore law, companies must update ACRA whenever there are changes to:- Company information (e.g. business activities, registered address, company name)

- Directors and company secretary details

- Shareholders and shareholding structure

- Personal particulars (e.g. name, address, identification details)

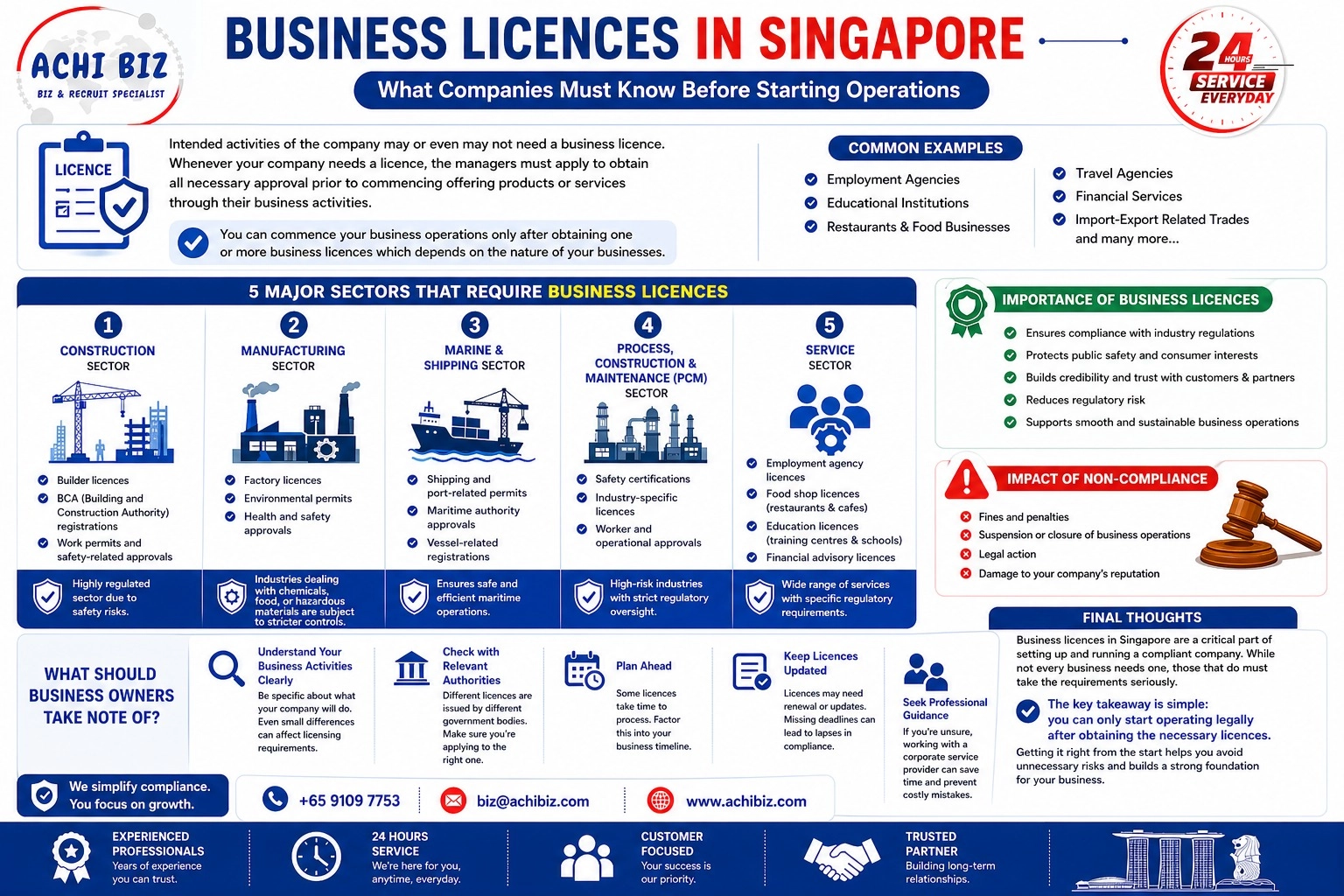

What Companies Must Know Before Starting Operations

Starting a private limited company (Pte Ltd) in Singapore is relatively straightforward—but that doesn’t mean you can begin operations immediately. One of the most overlooked areas is business licensing in Singapore. Depending on what your company intends to do, you may need one or more business licences before you can legally offer your products or services. Let’s break this down clearly so you know exactly what to expect.

Not every business requires a licence—but many do. Your company’s intended activities will determine whether a business licence in Singapore is required. If your business falls within regulated industries, you must obtain the relevant approvals before starting operations. Some common examples include employment agency licences, education licences, restaurant licences, travel agency licences, financial services licences, and import export licences. The key point is simple: if a licence is required, you cannot operate legally without it.

Notification of Changes / Updating Information

Running a Pte Ltd company in Singapore comes with ongoing responsibilities—and one of the most overlooked is keeping your company information and personal particulars of officers up to date.

This includes changes to directors, shareholders, company secretary, registered address, shareholding structure, and personal details such as residential address, passport number, or contact information.

It may sound administrative, but in reality, it’s a core compliance requirement under ACRA. Ignoring it can create serious issues down the line.

What Changes Must Be Updated?

Under Singapore law, companies must update ACRA whenever there are changes to:

- Company information (e.g. business activities, registered address, company name)

- Directors and company secretary details

- Shareholders and shareholding structure

- Personal particulars (e.g. name, address, identification details)

Even small changes—like updating a residential address—must be properly recorded.

Click here to learn more about updating information of entities / firms and officers / owners.

Business Licensing and Permits

Business Licensing and Permits

What Companies Must Know Before Starting Operations

Starting a private limited company (Pte Ltd) in Singapore is relatively straightforward—but that doesn’t mean you can begin operations immediately. One of the most overlooked areas is business licensing in Singapore. Depending on what your company intends to do, you may need one or more business licences before you can legally offer your products or services. Let’s break this down clearly so you know exactly what to expect.

Do All Businesses in Singapore Need a Licence?

Not every business requires a licence—but many do. Your company’s intended activities will determine whether a business licence in Singapore is required. If your business falls within regulated industries, you must obtain the relevant approvals before starting operations. Some common examples include employment agency licences, education licences, restaurant licences, travel agency licences, financial services licences, and import export licences. The key point is simple: if a licence is required, you cannot operate legally without it.

Registered Office and Working Hours

Every Singapore Company is required to have a registered office in Singapore to which all communication and notices may be addressed and which shall be open and accessible to the public for at least 3 hours a day during regular business hours on weekdays.

Alternate Address

Directors and company officers have the option of providing ACRA with an address in addition to their usual residential address. The alternate address will be displayed in the Business Profile for public information, instead of the residential address. It must be an address where the company officer can be contacted, and must be within the same jurisdiction as the residential address. It cannot be a P.O. Box address. This service is subject to fee payable to ACRA.

ACRA reserves the right to display the officer’s residential address in the Business Profile should this officer cannot be reached via his/her given alternate address.

ACRA reserves the right to display the officer’s residential address in the Business Profile should this officer cannot be reached via his/her given alternate address.

Customs Registration Number (CR)

Declaring Entities and individuals carrying on business under their full name that intend to engage in import and/or export activities in Singapore, or appoint a Declaring Agent to apply for Customs import, export and transhipment permits or certificates through TradeNet have to activate their entity’s Customs Account

A Declaring Entity refers to any importer, exporter, shipping agent, air cargo agent, freight forwarder, common carrier or other persons who wish to obtain a permit, licence, certificate or any other document or form of approval from Singapore Customs.

Only the Key Personnel such as the owner, partner or director whose record is registered with ACRA or the relevant UEN Issuance Agency can activate your entity’s Customs Account using his / her CorpPass or SingPass.

Goods and Services Tax (GST)

What is Goods and Services Tax (GST)?

The Goods and Service Tax or GST is comparable to the VAT or Value Added Tax found in many other countries. It is a consumption tax that applies to many of the domestic goods and services used in Singapore. The current rate of GST is 7%.

GST however does not apply to sale/lease of majority financial services and residential real estate in Singapore. Even export of goods and services used elsewhere (outside Singapore) is exempt from GST. In order to collect GST, suppliers are required to register with the Comptroller, GST. The Singapore Customs collects GST against any goods that are imported at the point of import.

If you are a supplier of goods/services having annual income exceeding or expected to exceed SGD1 million, it is mandatory to register with the Comptroller. If you are a supplier who does not fall into this income bracket, you can still apply for voluntary registration. In this case, the Comptroller determines whether to approve your registration or not. After voluntary registration, it becomes mandatory to remain so for at least two years.

GST Services by ACHI

GST services by ACHI helps make the process of registration, compliance and filing more convenient. We have experienced staff on GST services who help your Company with the following processes:

Registration for GST

ACHI applies for registration of GST on your Company’s behalf with the Inland Revenue Authority of Singapore [IRAS]. We will follow up with all the queries with regard to the registration.

Filing of GST Return

We provide an assessment for determining the effect of GST registration on your business and customers. We will provide recommendations based on this assessment for the ideal GST filing period for your business. You can take advantage of our bi-annual or quarterly GST filing services.

Click here to learn more from IRAS e-Tax Guide about “How do I prepare my GST Return”.

Click here to learn more about GST (Goods And Services Tax) in Singapore.

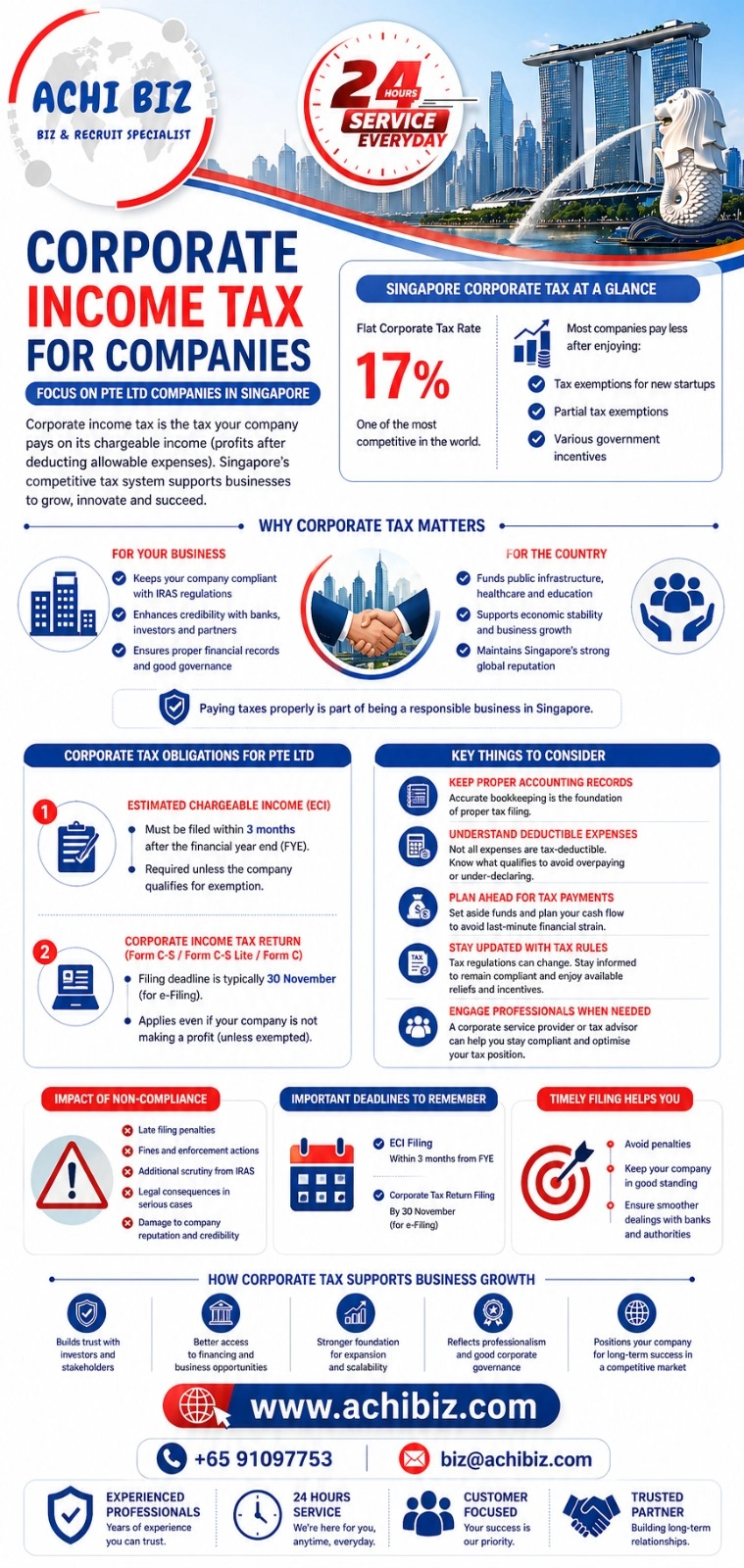

Singapore Corporate Income Tax (CIT)

The corporate tax rate is at 17% currently. Tax will only be imposed at the corporate level and Singapore dividends in the hands of the company’s shareholders are tax exempt.

What Is Corporate Income Tax in Singapore?

Corporate income tax is the tax your company pays on its chargeable income, which is essentially your profits after deducting allowable expenses.

In Singapore, the corporate tax rate is 17%, but most companies pay less due to:

- Tax exemptions for new startups

- Partial tax exemptions

- Various government incentives

This makes Singapore one of the most business-friendly tax environments globally.

General Rule of Corporate Income Tax for All Companies

A company is taxed on the income earned in the preceding financial year. This means that income earned in the financial year 2018 will be taxed in 2019.

Corporate Income Tax Filing Obligations to all Companies

All companies are required to submit two corporate income tax forms to IRAS every year:

|

Name of Taxation Form

|

Due Date

|

|---|---|

|

Estimated Chargeable Income (ECI)

|

Within 3 months from the end of financial year, unless the company does not need to submit ECI

|

|

Form C-S (or) Form C online

|

Every 15th December

|

Click here to learn more about Singapore Corporate Income Tax.

Withholding Tax In Singapore

A withholding tax is an income tax to be paid to the Government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient.

Overview of Withholding Tax in Singapore

Under the law, a person (known as the payer) who makes payment(s) of a specified nature (e.g. Royalty, Interest, Technical Service Fee, etc.) to a non-resident company or individual person (known as payee) is required to withhold a percentage of that payment and pay the amount withheld (called ‘Withholding Tax’) to the tax authority viz. IRAS.

From 1 Jul 2016, the withholding tax form can only be filed electronically via myTax Portal. The payer must e-file and pay the withholding tax to IRAS by the 15th of the second month from the date of payment to the non-resident.

To find out the percentage to withhold, you can refer to below Types of Payment and the Applicable Withholding Tax Rates.

Click here to learn more about Withholding Tax in Singapore.

Membership with Singapore Business Federation (SBF)

Under the SBF Act, all Singapore-registered companies with share capital of S$0.5 million and above are members of SBF. Companies registered with ACRA with paid-up capital that meets the threshold of $0.5 million will receive a notification letter from SBF on their membership.

For more information, please visit the SBF website at www.sbf.org.sg

Other Compliance

Other Compliance will be applicable according to your type of entity, nature of businesses and licences hence you are required to seek the Professional Corporate Secretarial Service Provider like ACHI for further assistance on your requirements.

Please CONTACT us if you wish to know about these or many other services