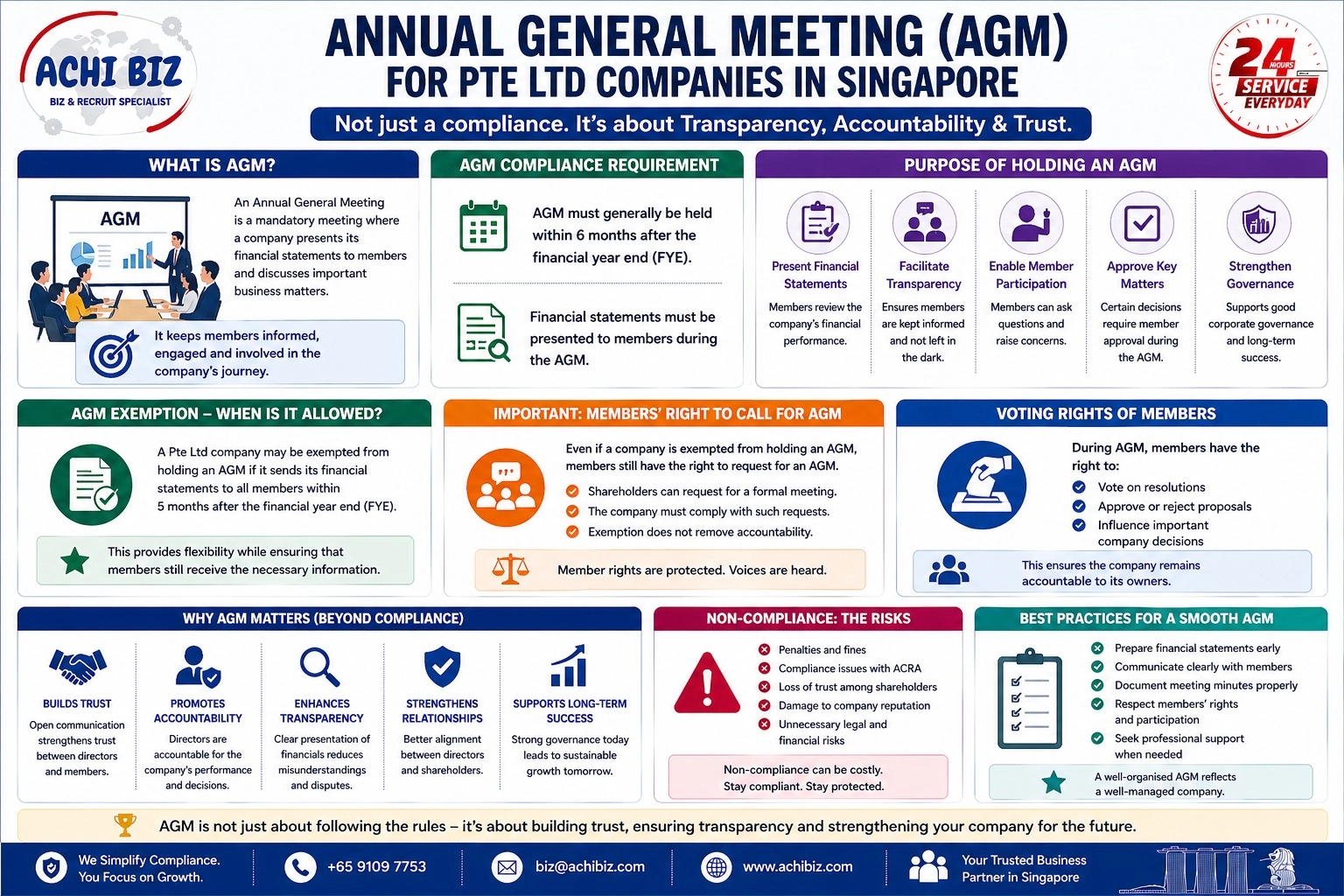

During an AGM, the company presents its financial statements to members, and answers any queries on the business.

AGMs are conducted under the direction of the chairman of the meeting, who is usually the chairman of the board of directors. If your company’s Constitution does not specify a chairman to regulate the meeting, any member can be elected at the AGM to fulfil the role.

The company secretary – or an appointed secretarial service – is required to prepare any necessary documentation for the AGM (e.g. the company Constitution).

Please take note of the following when AGM is conducted.

Other than ordinary business, the meeting should only deal with resolutions for which notice has been given.

Ordinary business is defined in your company’s Articles, and may include subjects such as:

- Dividend pay-outs

- Appointment of directors/auditors

- Remuneration for senior executives and directors

- Consideration of accounts and balance sheets

Subjects other than these may be considered special business.

Any resolutions at the meeting, other than ordinary business, should have been mentioned in the Notice of the AGM.

[Note] If you vote on a topic that was not mentioned in the notice, the resolution may not be legally valid. This is because a member with voting rights may be absent during the meeting, and have no knowledge of the matter.

Note that members also have the right to propose resolutions for the meeting. However, they must bear the expense of circulating such resolutions.

Quorum

The quorum is the minimum number of members who must attend the AGM, for it to be considered valid.

If the quorum is not specifically stated in your company’s Constitution, the minimum number is two members (or their proxies).

Appointment of Proxies

A proxy can attend and vote on behalf of a member at the AGM. The proxy does not need to be a member of your company.

The procedure for appointment of a proxy should be in your company’s Constitution; the procedure may be applicable for all meetings, or only for the current meeting.

Ensure that the procedures have been followed by members using proxies.

Laying of Financial Accounts

Directors are responsible for presenting documents such as:

- Financial statements

- Balance sheets

- Director’s report

- Auditor’s report (if applicable)

These materials should also be sent with the Notice of the AGM, at least 14 days prior to the meeting. This will allow members to prepare questions for the directors.

Voting for Various Resolutions

Your company’s Constitution covers the voting rights of members, as well as the procedures for voting.

Usually, all members have the right to vote, barring exceptional circumstances (e.g. a member who has not paid up for shares issued to them, when notified by the company, may be denied the right the vote).

Voting is done by a show of hands or a poll; but note that proxies are usually not allowed to vote by a show of hands, unless the company’s Constitution allows this.

Closing of your AGM

The minutes of the AGM must be recorded in writing, and signed by the company’s chairman. The company must then file its Annual Returns with the Authority viz. ACRA.

When convening an AGM, you must send a written Notice of the AGM to all members. This includes:

- The estates of any deceased members

- The Official Assignee (OA) overseeing any bankrupt members’ affairs

- The current auditor of the company

- Any other persons specified in the company’s Articles

The minimum notice period is 14 days, though the Constitution may provide for a longer period of notice. The notice period can also be shortened, with the agreement of all the members entitled to attend and vote.

Details to include in the notice

- Date, time, and venue of the AGM

- Details of any resolutions to be passed

- Notice of a member’s right to appoint a proxy (for members who cannot attend in person)

- Ordinary business to be transacted

- Copies of the financial statements, balance sheet, and director’s or auditor’s report

Serving the notice to members

Notices may be served personally, by post, by e-mail and other forms of electronic communications, or by any other means permitted by the Constitution.

Special Notice

A special notice is required under certain circumstances, such as the removal of directors or auditors. Such a notice must be served to members at least 28 days before the date of the meeting.

Timeline for Holding AGM

Timeline for Holding AGM

For companies with financial year ending (FYE) on or after 31 August 2018:

If you are a listed company, you must hold an AGM within four months after your company’s financial year end and file the annual return within five months after your company’s financial year end.

If you are not a listed company, you must hold an AGM within six months after your company’s financial year end and file the annual return within seven months after your company’s financial year end.

For companies with financial year ending (FYE) before 31 August 2018:

You must hold the first AGM within 18 months of the date of incorporation.

The financial statements you present at an AGM must be made up to a date not more than four months before the AGM, if you are a listed company. For non-listed companies, it must be made up to a date not more than six months before the AGM.

Exemptions from holding an AGM

With effect from 31 August 2018, private companies can be exempted from holding AGMs if they send their financial statements to their members within five months after the financial year end.

The exemption to hold an AGM is subject to the following safeguards:

- A member who wishes to request that an AGM be held must notify the company no later than 14 days before the end of the sixth month after the financial year end

- Directors must hold an AGM within 6 months after the financial year end if notified by any member of the company to do so. The company may seek the Registrar’s approval for an extension of time to hold AGM by the deadline (i.e. before the end of the six months after the financial year end)

- Private companies must hold a general meeting to lay financial statements if any member or auditor requests for it no later than 14 days after the financial statements are sent out. Directors must, within 14 days after the date of request, hold a general meeting to lay the financial statements.

Private dormant relevant companies*, which are exempt from preparing financial statements, do not need to hold AGMs, subject to the above safeguards.

*A private dormant relevant company is a private company which is dormant, not listed (or not a subsidiary of a listed company); and has total assets less than or equal to $500,000 (consolidated value if it is an ultimate parent).

Dispensing with AGMs

A private company need not hold AGMs if all the members pass a resolution to dispense with the holding of annual general meetings. Companies may pass written resolutions for matters that would have been tabled at an AGM. The written resolutions may be circulated via hardcopies or other legible form (such as e-mails) as agreed upon by the company and the members.

Applying for an Extension of Time to hold your AGM

You can apply for an Extension of Time (EOT) of up to 60 days, if you need to delay holding the AGM or filing the annual return.

An EOT application can be made by a company officer (e.g. company secretary or director), or by a professional firm on behalf of your company.

- The application fee is $200.

- Provide the reasons for the application (Listed companies are to attach the reasons for the application, along with any relevant documents, including any comments by SGX on the application).

- Once the EOT application is successfully submitted, a confirmation email will be sent by ACRA to the person making the application.

Notification of AGM date after filing latest Annual Return (AR) without AGM

Notification of AGM date upon member request after latest AR was filed without AGM:

When any member is requesting the Company to hold AGM within the applicable due date after filing the Annual Return, the Company is required to notify the Registrar within 14 days from the date of AGM however it should be notified within the due date otherwise it will incur with late penalties by ACRA.

During the notification of AGM, the below information are required to be furnished:

- Date of AGM requested by member

Note: Notification of AGM Date is only applicable if the latest AR was filed without an AGM date.