A Firm is treated as general partnership until reasonable notice of

registration of LP

A Partnership (general) can also be converted into an LP where one or more

(but not all) of its partners register themselves as limited partners. The

resulting LP formed must also register itself as an LP under the Limited

Partnership Act. Where a person deals with a firm after it becomes an LP,

that person is entitled to treat the firm as a general partnership until he

has notice of the registration of that firm as an LP. He is also entitled to

treat any person who was a partner of the firm as a general partner of the

LP until he has notice of the registration of that person as a limited

partner.

Limited Partners

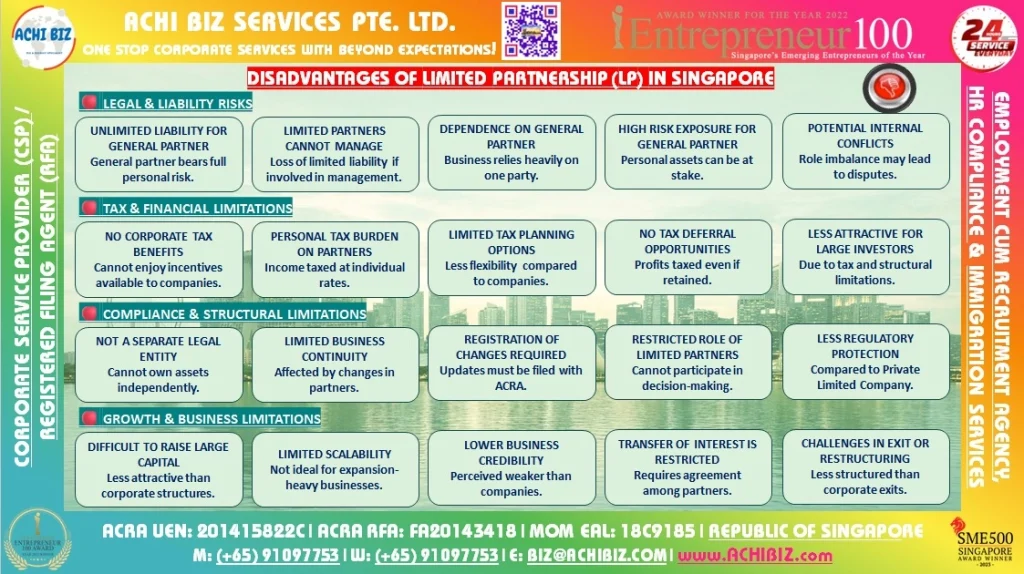

- Limited Partners are not liable for debts or obligations of firm beyond

agreed amount - The key difference between LPs and Partnerships lies in the fact that

LPs have ‘limited partners’. A limited partner is defined as any partner

who, under the terms of the partnership agreement, shall not be liable

for the debts or obligations of the firm beyond the amount of his agreed

contribution. - The limited partner is thus said to enjoy ‘limited liability’ status.

Anyone who is not a limited partner of an LP is a general partner.

General partners are regarded in exactly the same manner as partners in

a Partnership and are liable for all the debts and obligations of the LP

incurred while they are general partners.

Requirements of Registration under the Limited Partnerships Act

Parties who wish to be limited partners in an LP have to register themselves

as such under the Limited Partnerships Act. Failing to do so will result in the limited partners being treated as if

they were general partners of the LP. They will thereby lose their limited

liability status. Also, where a person deals with an LP after a partner

becomes a limited partner, that person is entitled to treat that partner as

a general partner of the LP until he has notice of the registration of that

partner as a limited partner.

Limited Partners are not to take part in management of the Limited

Partnership

Limited partners should not take part in the management of the LP and should

not have the power to bind the LP. Limited partners who take part in the

management of the LP are liable for all debts and obligations of the limited

partnership incurred while they so take part in the management as though

they were general partners.

Limited partners may vary contributions

Limited partners may increase, reduce or draw out their contributions with

the approval of the general partners, subject to the LP agreement.

When capital or Profits Distribution need to be Refunded?

Any distribution of capital or profits to the limited partners must be

refunded if the following conditions are present:

- Every general partner of the LP was insolvent at the time of the

distribution or became insolvent as a result of the distribution; - The limited partner knew or ought to have known at the time of the

distribution that every general partner was insolvent or would become

insolvent as a result of the distribution; and - Every general partner is adjudicated bankrupt or is ordered to be wound

up within one year after the date of the distribution.

Dissolution of Limited Partnership (LP)

- The dissolution of LPs is similar to that for Partnerships (General).

There are, however, some differences which relate to limited partners.

For example, limited partners are not entitled to dissolve the LP by

notice. Also, an LP is not dissolved on the death, dissolution,

bankruptcy or liquidation of a limited partner. - In the event of the dissolution of an LP, its affairs are to be wound up

by the general partners unless there is a court order to the contrary.

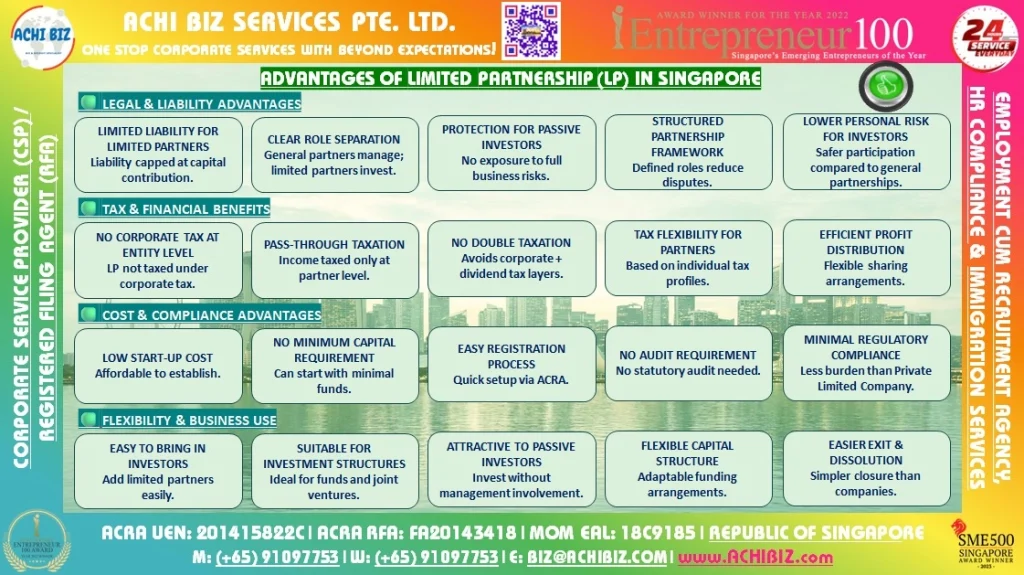

- Tax benefits: As with a general partnership, the

profits and losses in a limited partnership flow through the business to

the partners, all of whom are taxed on their personal income tax

returns. The difference is that the limited partners in the relationship

get to share in the profits and losses, but they do not have to

participate in the business itself. - Liability limits: A limited partner’s liability for the

partnership’s debt is limited to the amount of money or property that

individual partner contributed to the partnership. This is not true of

the general partnership, where any money or property contributed becomes

an asset of all the partners. - The general partners take charge: In a limited

partnership, the general partners deal with the daily operations and

responsibilities and don’t need to consult the limited partners for most

business decisions. - No turnover issues: Limited partners can be replaced or

leave without dissolving the limited partnership. - Less paperwork: Creating a limited partnership, like a

general partnership, requires less paperwork than forming a corporation.

However, it’s important to create and file a partnership agreement in

the county where your company does business. - Investment opportunities: A limited partnership is a

great way to offer investors the opportunity to benefit from the profits

and losses of your business without getting them actually involved in

the business.