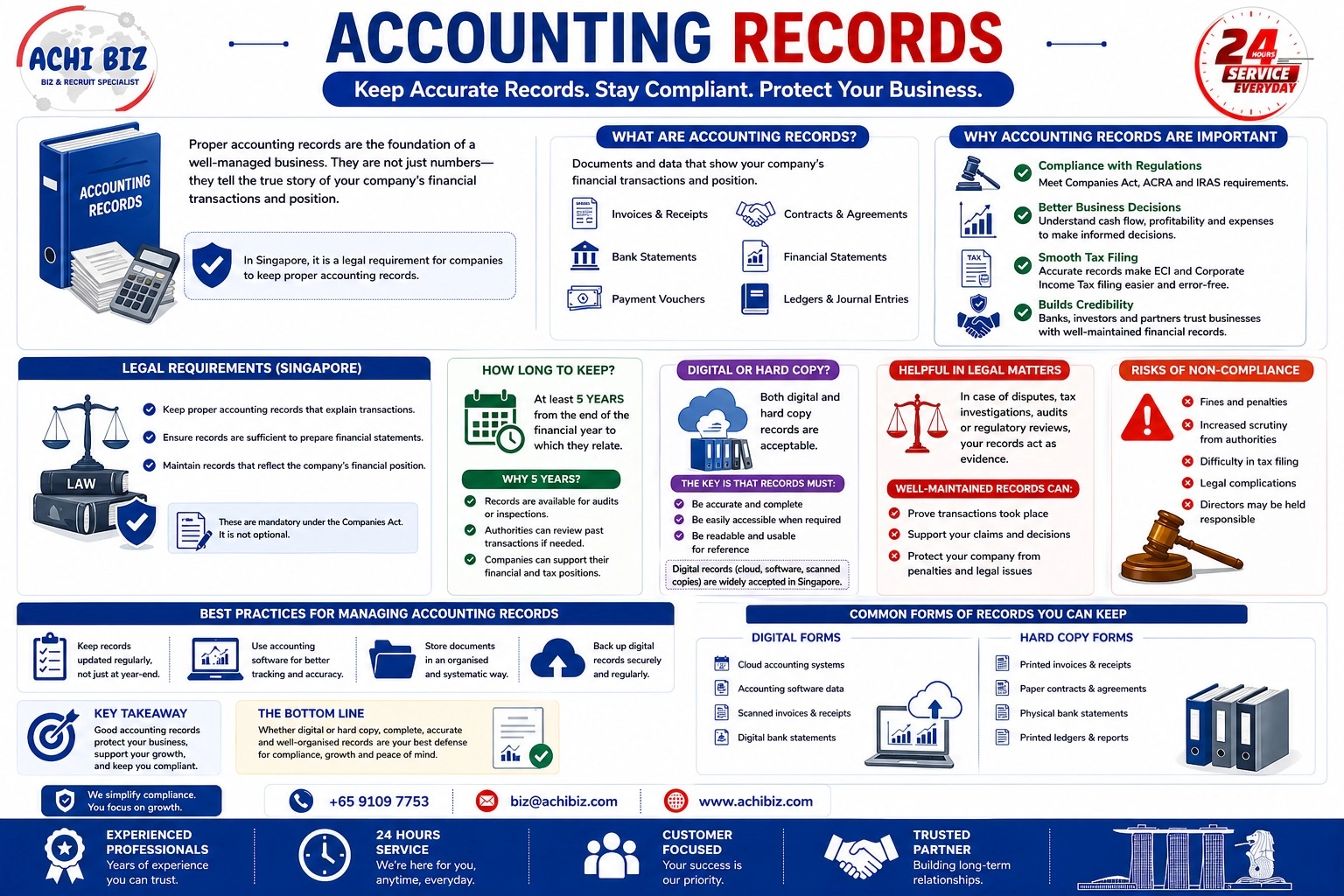

Why They Matter and How to Keep Them Properly

If you run a private limited company (Pte Ltd) in Singapore, keeping proper accounting records isn’t just good practice—it’s a legal requirement.

Many business owners only think about accounting when it’s time for tax filing. But in reality, well-maintained records play a much bigger role in your business—from compliance to decision-making and even protecting you during disputes.

Let’s break it down in a simple and practical way.

What Are Accounting Records?

Accounting records are the documents and data that show your company’s financial transactions and position.

These typically include:

- Invoices and receipts

- Bank statements

- Payment vouchers

- Contracts and agreements

- Financial statements and ledgers

In short, they tell the full story of your business finances.

Why Are Accounting Records Important?

Keeping proper accounting records in Singapore is not just about staying organised—it directly impacts your business in several ways.

Compliance with Regulations

Under the Companies Act, companies must maintain proper records that accurately reflect their transactions and financial position. This ensures you meet ACRA and IRAS requirements.

Better Business Decisions

Clear financial records help you understand your cash flow, profitability, and expenses. This allows you to make informed decisions instead of guessing.

Smooth Tax Filing

Accurate records make it easier to prepare tax filings like Estimated Chargeable Income (ECI) and Corporate Income Tax Returns without errors.

Builds Credibility

Banks, investors, and partners rely on your financial records to assess your business. Well-maintained records build trust and confidence.

Legal Requirements for Keeping Accounting Records

In Singapore, companies are required to:

- Keep proper accounting records that explain transactions

- Ensure records are sufficient to prepare financial statements

- Maintain records that reflect the company’s financial position

These are not optional—they are mandatory under the law.

How Long Should Accounting Records Be Kept?

This is one of the most common questions.

In Singapore, companies must keep accounting records for at least 5 years from the end of the financial year to which they relate.

Why 5 Years?

This requirement ensures that:

- Records are available for audits or inspections

- Authorities can review past transactions if needed

- Companies can support their financial and tax positions

Destroying records too early can create serious compliance risks.

Can Accounting Records Be Kept Digitally?

Yes—digital record keeping is allowed in Singapore.

You can maintain your accounting records in:

- Electronic format (cloud systems, accounting software)

- Scanned copies of physical documents

- Hard copy (paper documents)

The key requirement is that records must:

- Be accurate and complete

- Be easily accessible when required

- Be readable and usable for reference

Many companies today prefer digital records because they are easier to manage and retrieve.

How Accounting Records Help in Legal Matters

This is where proper records become extremely valuable.

In the event of:

- Disputes with customers or suppliers

- Tax investigations

- Audits or regulatory reviews

Your accounting records act as evidence.

Well-maintained records can:

- Prove transactions took place

- Support your claims and decisions

- Protect your company from penalties or legal issues

Without proper documentation, it becomes much harder to defend your position.

Common Mistakes to Avoid

Many companies run into issues due to simple mistakes:

- Not recording transactions promptly

- Losing receipts or invoices

- Keeping incomplete or inconsistent records

- Relying on memory instead of documentation

- Not backing up digital records

These may seem small, but they can lead to bigger problems during audits or reviews.

Best Practices for Managing Accounting Records

To stay on the safe side:

- Keep records updated regularly, not just at year-end

- Use accounting software for better tracking

- Store documents in an organised system

- Back up digital records securely

- Engage professionals if needed

A little discipline goes a long way.

Impact of Non-Compliance

Failing to maintain proper accounting records in Singapore can lead to:

- Fines and penalties

- Increased scrutiny from authorities

- Difficulty in tax filing

- Legal complications

In serious cases, directors may be held responsible for non-compliance.

Final Thoughts

Accounting records are more than just paperwork—they are the foundation of a well-managed business.

The key takeaway is simple:

Good accounting records protect your business, support your growth, and keep you compliant.

Whether you keep them digitally or in hard copy, what matters most is accuracy, completeness, and consistency.

If you stay organised and follow the rules, managing your accounting records becomes much easier—and far less stressful in the long run.