Dormant Pte Ltd Company in Singapore: ACRA, Audit Exemption, FS Exemption & IRAS Criteria Explained

If your private limited company (Pte Ltd) in Singapore is not actively operating, it may be considered a dormant company. While this can reduce compliance requirements, many business owners misunderstand what “dormant” actually means—and what obligations still remain.

Here’s a clear and practical guide to help you understand the rules under ACRA, audit exemption, financial statements (FS), and IRAS.

What Is a Dormant Company?

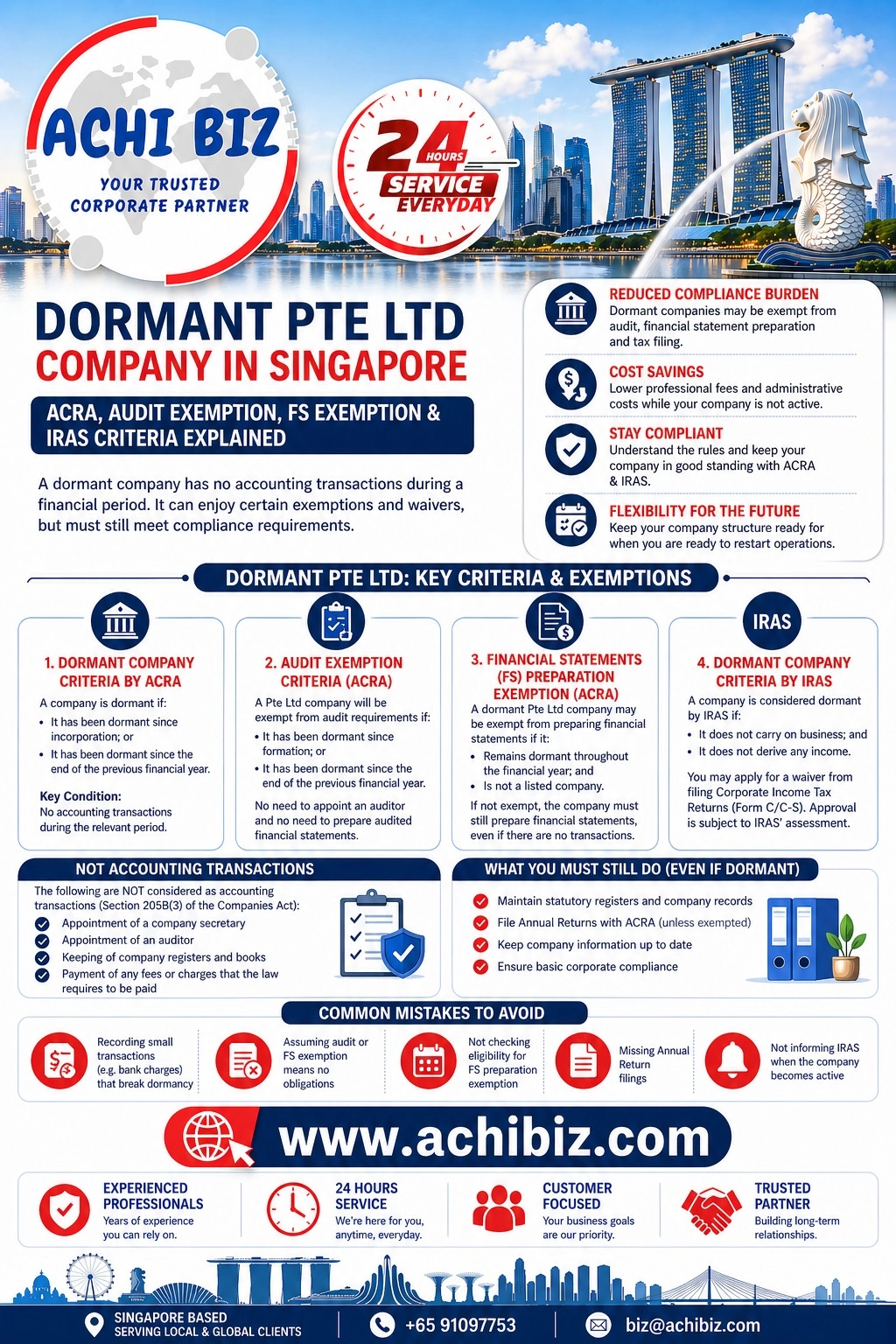

A company is considered dormant when there are no accounting transactions during a financial period. In simple terms, the company is not carrying out any business activities that involve money.

However, not every activity counts as an accounting transaction. Under Section 205B of the Companies Act, certain routine compliance actions are allowed without affecting dormant status.

These include:

- Appointment of a company secretary

- Appointment of an auditor

- Maintaining statutory registers and company records

- Payment of statutory fees or charges required by law

So, your company can remain dormant while still fulfilling basic compliance obligations.

ACRA Criteria for Dormant Pte Ltd Companies

Under ACRA, a Pte Ltd company is considered dormant if:

- It has been dormant since incorporation, or

- It has been dormant since the end of the previous financial year

The key condition is straightforward—no accounting transactions during the relevant period.

Once any transaction occurs, even a small one, the company will no longer be considered dormant.

Audit Exemption for Dormant Companies

Dormant companies benefit from audit exemption.

A Pte Ltd company will be exempt from audit requirements if:

- It has been dormant since formation, or

- It has been dormant since the end of the previous financial year

This means:

- No need to appoint an auditor

- No requirement to prepare audited financial statements

However, this only applies as long as the company remains fully dormant.

Financial Statements (FS) Preparation Exemption

Dormant companies may also qualify for exemption from preparing financial statements, which can significantly reduce compliance work.

For a Pte Ltd company:

- If it remains dormant throughout the financial year, it may not need to prepare a full set of financial statements

- This simplifies reporting obligations

However, if the company does not meet the exemption conditions, it must still:

- Prepare financial statements, even if there are no transactions

So, it’s important not to assume this exemption automatically applies—eligibility must be met.

IRAS Criteria for Dormant Companies

IRAS has its own definition of dormancy.

A company is considered dormant by IRAS if:

- It does not carry on business, and

- It does not earn any income

If your company meets these conditions, you may apply for:

- Waiver from filing Corporate Income Tax Returns (Form C/C-S)

However:

- Approval is subject to IRAS assessment

- Filing may still be required in certain situations

Once your company becomes active again:

- You must inform IRAS

- Tax filing obligations will resume

What You Must Still Do (Even If Dormant)

Even if your company is dormant, compliance does not stop completely.

You are still required to:

- Maintain statutory registers and company records

- File Annual Returns with ACRA (unless exempted)

- Keep company information updated

- Ensure basic corporate compliance

Dormant status reduces workload—but it does not remove responsibilities.

Common Mistakes to Avoid

Many companies lose their dormant status or face compliance issues due to simple mistakes:

- Recording minor transactions such as bank charges

- Assuming audit exemption means no obligations at all

- Not checking eligibility for FS preparation exemption

- Missing Annual Return filings

- Forgetting to notify IRAS when business resumes

Even small oversights can lead to penalties or compliance issues.

When Should You Keep a Company Dormant?

Keeping a company dormant can make sense if:

- You plan to restart the business in the future

- You want to retain the company structure

- Operations are temporarily paused

However, if there are no future plans, it may be more practical to consider striking off the company instead of maintaining ongoing compliance.

Final Thoughts

A dormant Pte Ltd company in Singapore can benefit from audit exemption and possible FS preparation exemption, making it easier to manage. However, these benefits come with strict conditions.

The key takeaway is simple:

Dormant does not mean inactive in compliance—it simply means no business transactions.

As long as you understand the requirements under ACRA and IRAS and keep your company in good standing, managing a dormant company can be straightforward and cost-effective.

Frequently Asked Questions (FAQs) on Dormant Pte Ltd Company in Singapore

What is a dormant company in Singapore?

A dormant company is a Pte Ltd company that has no accounting transactions during a financial year. This means it is not carrying out any business activities involving income or expenses.

What does ACRA consider as a dormant company?

ACRA considers a company dormant if it has no accounting transactions since incorporation or since the end of the previous financial year. Once any financial transaction occurs, the company is no longer dormant.

What transactions do not affect dormant status?

Certain activities are not considered accounting transactions, such as appointing a company secretary or auditor, maintaining company records, and paying statutory fees required by law.

Do dormant companies need to appoint an auditor?

No, a dormant Pte Ltd company is generally exempt from audit requirements if it has been dormant since incorporation or since the previous financial year.

Are dormant companies required to prepare financial statements?

Not always. A dormant company may be exempt from preparing financial statements if it meets ACRA’s criteria. If not exempted, it must still prepare financial statements even with no transactions.

Does a dormant company need to file Annual Returns?

Yes, in most cases, dormant companies are still required to file Annual Returns with ACRA unless specifically exempted.

What is IRAS’ definition of a dormant company?

IRAS considers a company dormant if it does not carry on business and does not earn any income during the financial year.

Do dormant companies need to file tax returns in Singapore?

Dormant companies may apply for a waiver from filing Corporate Income Tax Returns (Form C/C-S). However, approval is subject to IRAS and not automatic.

What happens if a dormant company starts business again?

Once the company has any accounting transaction, it is no longer dormant. It must resume normal compliance, including tax filing and financial reporting.

What are common mistakes when managing a dormant company?

Common mistakes include recording small transactions (like bank charges), missing Annual Return filings, assuming all obligations are waived, and failing to inform IRAS when the company becomes active.

Can a dormant company remain registered indefinitely?

Yes, as long as it continues to meet compliance requirements. However, if there are no future plans, striking off the company may be more practical.

Is maintaining a dormant company completely cost-free?

No. While costs are lower, you may still incur fees for corporate secretarial services, filing obligations, and statutory compliance.

💼 Contact us to manage your dormant company or stay compliant.